Quantitative Tightening: What is it and How Does it Work?

During the pandemic alone, the U.S. Federal Reserve bought a whopping $3.3 trillion in Treasury bonds and $1.3 trillion in mortgage-backed securities to lower borrowing costs. The reverse process, quantitative tightening (QT), where central banks reduce balance sheets, is much rarer. The Fed is the only central bank that has actually made such an attempt, but it had to stop abruptly in 2019 because of market turmoil. So the asset reduction plan would take the central bank into relatively uncharted territory.

As we know, officials like to downplay the importance of QT. As Fed Chair, Janet Yellen compared the process to watching paint dry. Jerome Powell, her successor, believes that QT will work in the background. In reality, it resembles dismantling an auxiliary economic mechanism having only vague ideas about the consequences.

With inflation and quantitative tightening making headlines and being a major topic of discussion among investors and traders, it's time for us to get to the bottom of this as well. Today we will learn what QT is, what its goals are, and how it will affect the markets.

How Quantitative Tightening Works

Quantitative tightening is quantitative easing in reverse. Instead of building reserves (owned by the private sector) by buying bonds, the Central Bank reduces reserves by refusing to reinvest as the bonds mature. The three channels through which QE is implemented also work in the opposite direction. First, QT sends a signal of an impending rate hike. Notably, market rates rose sharply precisely in early January, when the Fed was discussing a faster approach to QT than many had expected.

The second channel, the direct impact of QT on yields, involves presumptive calculations. Some analysts believe the Fed will reduce the balance sheet by $3 trillion over the next three years (bringing it to about 20% of GDP from the current 36%). Bank of America's Mark Cabana thinks this is comparable to a rate hike somewhere between a quarter point and 1.25%: a surprisingly wide range.

Powell also noted the uncertainty about QT: "Frankly, we have a much better understanding of how financial conditions are affected by rate hikes.”

When interest rates rise, the Fed raises rates on overnight loans, which then spread along the yield curve. In the case of QT, the impact is mainly on long-term yields. According to some economists, such as Kristin Forbes of the Massachusetts Institute of Technology, this means that QT could be a more powerful tool than raising rates because it would target hot segments of the credit market, such as mortgages. The Fed has said that the main tool will be a rate hike. However, if QT does affect longer-term yields, less rate hikes may be needed to fight inflation.

The last channel is liquidity. As the Fed buys fewer bonds, there may be fewer deals overall. Indeed, the Bloomberg index, which reflects the comfort of Treasury bond trading, recently rolled back to levels last seen at the beginning of the pandemic. This is reminiscent of the failed last round of QT, which ended in a liquidity crisis in the overnight credit market. But this time, the Fed is better prepared. For starters, there's a lot more money in the market. The Fed also created an overnight lending facility that will allow banks to get funds when needed.

What Are the Objectives of Quantitative Tightening?

QT has several principal goals, including:

- Reducing the amount of money in circulation (deflationary);

- Increasing the cost of borrowing along with raising the benchmark interest rate;

- Cooling an overheated economy without destabilizing financial markets.

QT can be accomplished by selling bonds in the secondary Treasury market, and if the supply of bonds increases significantly, the yield or interest rate needed to attract buyers tends to rise. Higher yields increase the cost of borrowing and reduce the appetite of corporations and individuals who previously borrowed money when lending terms were generous, and interest rates were close (or zero). Less borrowing leads to less spending, which leads to less economic activity, which theoretically leads to a cooling of asset prices. In addition, the bond-selling process removes liquidity from the financial system, forcing businesses and households to be more careful in their spending.

Quantitative Tightening vs. Tapering

Tapering is a term that is often associated with the quantitative tightening process, but actually describes a transitional period between QE and QT, when large-scale asset purchases are reduced or "contracted" before stopping altogether. During quantitative easing, proceeds from maturing bonds are typically reinvested in new bonds, injecting even more money into the economy. However, tapering is a process in which reinvestments are reduced and eventually stopped.

The term "tapering" is used to describe small additional asset purchases that do not "tighten," but simply reduce the rate at which assets are bought by central banks. For example, you wouldn't call taking your foot off the gas pedal a brake, even if the car starts to slow down, assuming you are driving on a smooth road.

Examples of Quantitative Tightening

Since quantitative easing and quantitative tightening are fairly modern policy tools, there are really not many opportunities to study QT. The Bank of Japan (BoJ) was the first central bank to apply QE but was never able to implement QT because of persistently low inflation.

Unlike the ever-repeating cycles of rising and falling rates, central bank balance sheet contractions have occurred only once in the history of global financial markets. As such, the impact of QT on the economy and markets is much less understood, and economists, analysts, and companies cannot put it into their models.

The Fed's balance sheet reduction began in October 2017, and over the next three months, the value of stocks and bonds around the world fell markedly. As early as a year after the QT began, market participants were debating whether the Fed had gone too far in shrinking the balance sheet: rates had risen significantly, making it harder to lend.

The dollar has strengthened, putting more pressure on emerging market borrowers with currency-denominated debt. Emerging-country bond premiums rose, as did high-yielding U.S. bonds.

Finally, after the S&P 500 index fell 16% over three weeks in December 2018, the Fed decided to adjust its plans: rate hikes ended in January 2019, and QT in March.

As you can see, the process is largely untested as the program was cut.

Potential Shortcomings of Quantitative Tightening

Implementing QT involves striking a delicate balance between taking money out of the system and keeping financial markets stable. Central banks risk removing liquidity too quickly, which could spook financial markets, leading to volatile movements in the bond or equity market. This is exactly what happened in 2013, when Federal Reserve Chairman Ben Bernanke simply mentioned the possibility of a slowdown in future asset purchases, causing Treasury yields to spike, leading to lower bond prices.

Such an event is called "tapering hysteria" and can still manifest itself during the QT period. Another disadvantage of QT is that it was never completed. Quantitative easing was implemented after the global financial crisis in an attempt to cushion the deep economic downturn that followed. Instead of tightening after Bernanke's comments, the Fed decided to implement a third round of quantitative easing until just recently, in 2018, the Fed began the quantitative easing process. Thus, the only example that can be cited suggests that the future implementation of QT may well result in negative market conditions again.

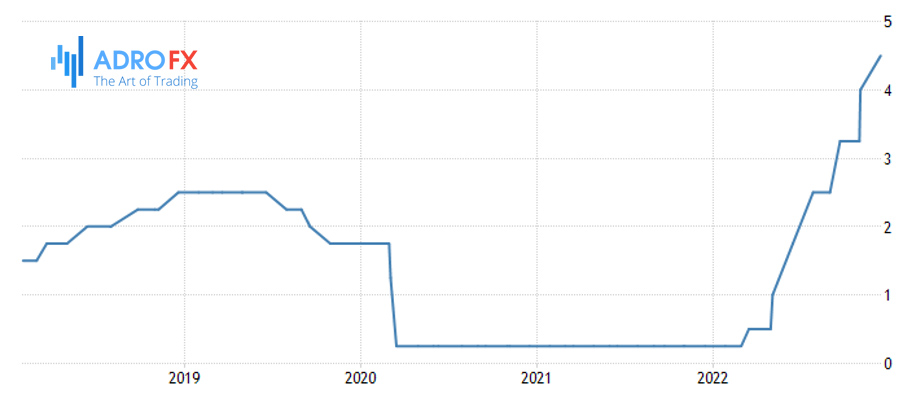

The Fed began raising the rate in March 2022, from about zero (0-0.25%), the first time it has done so since 2018. In parallel, since June, it has been implementing QT - selling off mortgage and treasury bonds from the balance sheet to remove "excess" liquidity from the market amid a run-up in inflation.

At the same time, the Fed and its head Jerome Powell are criticized for not reacting to price increases long enough, considering higher inflation a temporary phenomenon, and now a sharp tightening of monetary policy could lead to a recession. Recent economic reports point to a slowing U.S. economy and a cooling labor market that suggests steep interest-rate hikes by the Federal Reserve are starting to have a broader impact.

How Does the Current QT Differ?

After the surge in U.S. Treasury bond yields in 2013, the regulator is trying to communicate its intentions to the markets in advance: the Fed announced the imminent release of the QT plan this time back in late January. Jerome Powell also made it clear that it could happen faster than in 2017-2019 when the maximum amount of balance sheet cuts was $50 billion.

That said, the QT of 2018, which was also known in advance, still had a negative impact on the markets - it is worth bearing in mind that it was almost twice as slow as the current one promises to be. Inflation was much lower then, and unemployment was higher, so the Fed had to act more cautiously.

Probably the key question for investors in the next few months is to what level the U.S. regulator can reduce its balance sheet. For example, some analysts think QT will reduce the Fed's balance sheet to about $5 trillion within a few years. History shows that the Fed can tighten monetary policy until something "breaks, "as per experts.

Of course, the Fed has concluded from experience and will not allow the size of assets on the balance sheet to fall below what is necessary to maintain the functioning of the money market. In addition, now the banks have more than $5 trillion in reserves, including $1.8 trillion received on reverse REPO transactions with the Fed, so there should be no problems with liquidity in the money market even in case of rising rates.

How Will QT Affect the Markets?

The quantitative impact of QT on markets is difficult to account for. But given that since the global financial crisis and the first QE, the S&P 500 Index has directly correlated with the size of the Fed's balance sheet, it is clear why investors fear the beginning of its reduction. Even a reduction in the parameters of quantitative easing can have an impact on markets. This put pressure on the economy and, especially, the housing market, forcing the Fed to postpone plans limiting balance sheet growth.

The Fed's signals and anticipation of rising rates and the beginning of the regulator's balance sheet reduction have already led to the fact that the U.S. bond market in 2022 was the worst in the last 40 years. Rates on short- and medium-term treasuries rose to their highest level in decades.

The stock market is also beginning to react to the beginning of a tightening of the Fed's policy:

As you can see on the chart, the S&P 500 index dropped 13% from the beginning of the year, and the Nasdaq 100, which includes more sensitivity to the change of rates - by 27%. But the markets haven't yet fully accounted for the impact of QT.

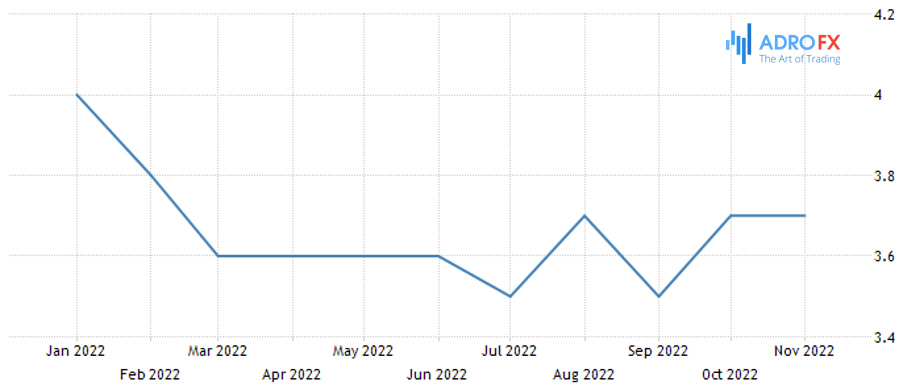

The risk with QT is that the Fed may be underestimating how much a balance sheet reduction would worsen financial conditions. According to the Fed, a balance sheet reduction would have been the equivalent of one 0.25-point rate hike, while Deutsche Bank expects a projected $1.9 trillion balance sheet reduction from 2022-2023 to be the equivalent of a 1-point rate hike. As we can see, there were 4 consecutive 0.75% rate hikes:

In the negative scenario which we witness right now, tech stocks were the first to suffer - their valuations are more dependent on expectations about the future. In addition, the recent decline in banking sector stocks reflected the growing risk of increased credit losses.

In 2022, global market liquidity will shrink by $2 trillion, half of which will come from the Fed - leading to a decline in overvalued stocks, Morgan Stanley warned in February. The investment bank advised investors to pay attention to stocks of quality growth companies that could be bought at fair prices and to strengthen geographical diversification, including stocks of companies outside the U.S. in their portfolios.

The Fed's soft policies have led to company valuations becoming a function of a few investor beliefs:

- there is no alternative to stocks;

- FOMO, the fear of missing out;

- BND, buy the dip.

The Fed's balance sheet cuts could put an end to this triad.

Conclusion

How exactly the Fed will reduce the balance sheet is an important signal, because selling bonds could have a greater negative impact on markets in case of liquidity problems. As a result, the prices of securities will fall harder, leading to an increase in mortgage bond rates and could hit the housing market.

About AdroFx

Established in 2018, AdroFx is known for its high technology and its ability to deliver high-quality brokerage services in more than 200 countries around the world. AdroFx makes every effort to keep its customers satisfied and to meet all the trading needs of any trader. With the five types of trading accounts, we have all it takes to fit any traders` needs and styles. The company provides access to 115+ trading instruments, including currencies, metals, stocks, and cryptocurrencies, which make it possible to make the most out of trading on the financial markets. Considering all the above, AdroFx is the perfect variant for anyone who doesn't settle for less than the best.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates