Potential Effects of Fed Rate Cuts on the Financial Landscape

While the Federal Reserve chose to maintain interest rates on Wednesday, a subtle shift in tone suggests the possibility of the first rate cut in four years, potentially scheduled for March. A noteworthy development is the removal of language from the Federal Open Market Committee's (FOMC) statement regarding the possibility of higher rates, indicating a significant shift in the Fed's stance on future rate actions. However, the committee remains cautious, asserting that rate cuts will not occur "until it has gained greater confidence that inflation is moving sustainably toward 2 percent." The impending first rate cut holds considerable weight, considering the broad impact of the Fed's previous rate hikes. Having raised benchmark interest rates from near zero in early 2022 to 5.25% to 5.50% by July 2023, the economy witnessed effects such as reduced inflation (the primary motive behind rate hikes), increased borrowing costs, a slowdown in the housing market, and rising bond yields. Should the anticipated rate cut materialize, it has the potential to reverse many trends observed over the past two years, offering a glimpse of economic shifts that are already underway in anticipation of the impending rate cuts.

Understanding the Federal Funds Rate

The federal funds rate serves as a key tool for the Federal Reserve to implement monetary policy and influence the overall health and stability of the economy. It represents the interest rate at which depository institutions (banks and credit unions) lend funds to each other overnight within the United States' banking system. Key points about the federal funds rate include:

- Overnight Lending Rate: The federal funds rate signifies the cost at which banks can borrow money from one another on an overnight basis to meet reserve requirements or manage daily operations.

- Monetary Policy Tool: Adjustments to the federal funds rate are part of the Federal Reserve's monetary policy to achieve its dual mandate: maximum sustainable employment and stable prices.

- Influence on Interest Rates: Changes in the federal funds rate have a ripple effect on other interest rates, impacting borrowing costs throughout the economy and stimulating economic activity when lowered.

- Open Market Operations: The Fed primarily influences the federal funds rate through open market operations, injecting or withdrawing money to adjust the rate.

- Impact on Economic Indicators: Analysts and policymakers closely monitor the federal funds rate as an indicator of the Fed's stance on monetary policy, with changes influencing economic indicators such as employment, inflation, and overall economic growth.

In summary, the federal funds rate is a crucial tool that the Federal Reserve uses to guide the economy by influencing borrowing costs and credit conditions. Adjustments to this rate play a significant role in shaping the overall financial environment and supporting the Fed's broader economic objectives.

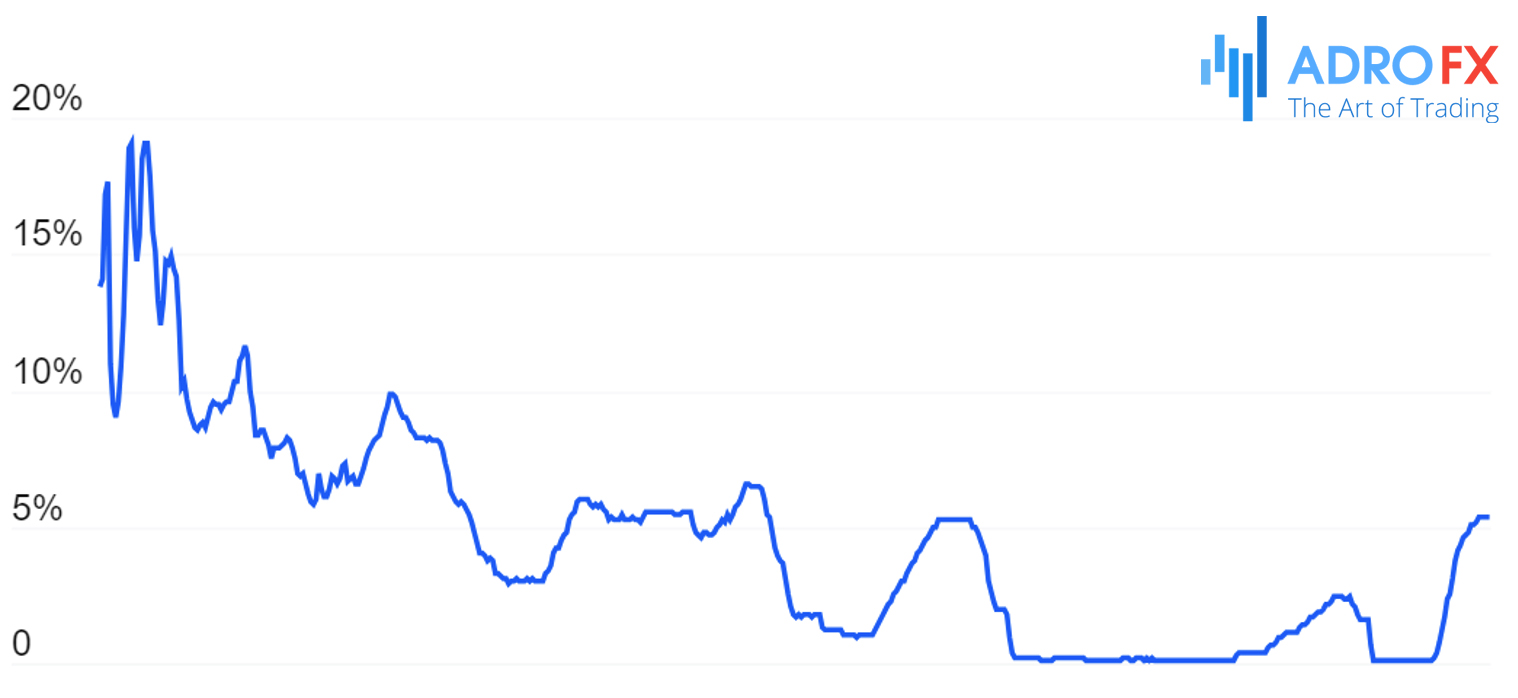

Overview of the Federal Funds Rate (1990-2024)

Examining the historical trajectory of the federal funds rate offers insights into the US monetary policy's response to various economic events over the past three decades. The key milestones include:

- Early 1990s Recession (1990-1993): The Fed lowered the fed funds rate from approximately 8.25% in 1990 to 3% by 1993 to combat rising unemployment after an eight-month recession.

- Dot-Com Boom and Bust (1995-2000): The late 1990s witnessed a rapid rise in the stock market, known as the "dot-com bubble." To stabilize the economy after the bubble burst in 2001, the Fed consistently cut rates, reaching around 1% in 2003.

- Housing Market Dynamics (2004-2008): Amid recovery from the dot-com fallout, worries of a housing bubble emerged, leading the Fed to raise rates to 5.25% in 2006. The housing market crash in 2008 prompted rate cuts, bringing the fed funds rate to 2% in April 2008.

- Great Recession (2008-2009): The housing market collapse triggered the Great Recession, prompting the Fed to reduce rates to 0%, where they remained until 2015.

- Post-Recession Period (2015-2019): Approximately six years after the Great Recession, the Fed gradually raised rates to a range of 2.25% to 2.5% before a slight cut in 2019, termed a "mid-cycle adjustment."

- COVID-19 Pandemic (2020): Despite the pandemic causing the shortest US recession (two months), emergency rate cuts were implemented, setting the range at 0% to 0.25%.

- Post-Pandemic Economic Rebound (2022-2023): In response to inflation reaching a 40-year high, the Fed initiated aggressive rate hikes starting in March 2022, reflecting efforts to stabilize the economy in the aftermath of the pandemic.

For a visual representation, refer to the federal funds rate chart history:

Mortgage Rates: A Downward Trend

While the Fed's rates aren't the sole factor influencing mortgage rates, they exert significant influence. Rate cuts typically lead to lower mortgage rates. Fannie Mae predicts that, by year-end, mortgage lenders might offer 30-year fixed-rate mortgages with average rates below 6%, nearly 2 percentage points lower than 2023 highs. This drop could stimulate home sales in 2024 as buyers find more affordable financing options. Homeowners with pre-2022 low-rate mortgages may feel less tied to their loans, potentially increasing housing inventory.

Savings Rates: An Expected Dip

In a high-interest rate environment, financial institutions offer better rates on products like high-yield savings accounts and CDs. However, with Fed rate cuts, these rates tend to decrease. Some online banks have already adjusted CD rates, and while high-yield savings account rates remain competitive, they are likely to drop in tandem with Fed rate cuts in 2024. Savers may see a reduction in opportunities to earn high APYs without taking on additional risk.

Auto Loans, Personal Loans, and More: Decreasing Rates

Auto loan rates, especially for used vehicles, reached over 7% and 11.6% in the last quarter of 2023, impacting affordability. Personal and student loan rates rose due to Fed hikes, and credit card APRs followed suit. However, a potential shift is expected with rate cuts in the coming months. Rates for auto loans, personal loans, and other financial products should decrease, offering consumers more affordable financing. Falling rates may also present opportunities for loan refinancing, allowing individuals to save on monthly payments.

Inflation Dynamics: A Delicate Balance

The Fed's focus on core prices reveals a 2.9% rate over the past 12 months, a notable improvement from the 5.6% peak in early 2022. On a six-month basis, core inflation slightly lags behind the Fed's 2% target. This decline in inflation provides an opportunity for the Fed to cut rates. However, the risk of cutting too soon looms large. A surge in spending following rate cuts could lead to accelerated price increases, a scenario the Fed aims to avoid. Potential buyers, inspired by better financing opportunities, may increase demand, potentially driving prices higher. The Fed's primary concern is a rebound in inflation, prompting caution in early 2024 as it continues monitoring the situation.

Stock Market Implications: Optimism Amid Uncertainty

Investors often express optimism about the prospect of Federal Reserve rate cuts, anticipating a boost to economic growth. However, an examination of historical data reveals a nuanced relationship between interest rate cuts and stock market performance.

In the past nine instances where the Federal Reserve paused its interest rate hikes and subsequently implemented rate cuts, the transitional pause period typically witnessed a surge in stock prices. Interestingly, once the actual rate cuts were initiated, the market did not favor investors.

On average, following the commencement of interest rate cuts, the stock market experienced a 23% decline in value. For investors with a $1 million stock portfolio, this could translate into a concerning reduction to $750,000. This underscores the importance of caution and the need to explore diversification strategies in anticipation of potential rate cuts.

In conclusion, while the allure of riding the wave of stock market excitement amid potential interest rate cuts is strong, it is crucial to base investment decisions on historical data and trends for long-term financial stability. Embracing a diversified approach that includes both stocks and bonds can safeguard wealth from the potential repercussions of rate cuts, ensuring the continual development of a resilient and successful investment portfolio.

Conclusion

In summary, the potential for the first Fed rate cut in four years signals a significant shift in the financial landscape. The removal of language regarding higher rates and the Fed's cautious stance indicate a pivotal moment. The historical trajectory of the federal funds rate highlights the Fed's response to economic events from the 1990s to the post-pandemic rebound in 2022-2023.

The article explores potential effects, including a downward trend in mortgage rates, a dip in savings rates, and decreasing rates for auto loans and personal loans. The delicate balance in inflation dynamics is noted, with the Fed focusing on core prices. Stock market implications suggest optimism amid uncertainty, anticipating upward pressure on stock prices due to quicker-than-expected rate cuts.

As the financial landscape awaits these potential shifts, the Federal Reserve's cautious monitoring of inflation and economic indicators reflects a commitment to its dual mandate. The intricate interplay between monetary policy, economic indicators, and market reactions will shape the trajectory of the financial landscape in the foreseeable future.

About AdroFx

Established in 2018, AdroFx is known for its high technology and its ability to deliver high-quality brokerage services in more than 200 countries around the world. AdroFx makes every effort to keep its customers satisfied and to meet all the trading needs of any trader. With the five types of trading accounts, we have all it takes to fit any traders` needs and styles. The company provides access to 115+ trading instruments, including currencies, metals, stocks, and cryptocurrencies, which make it possible to make the most out of trading on the financial markets. Considering all the above, AdroFx is the perfect variant for anyone who doesn't settle for less than the best.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates