Financial Crisis 2008 Explained: Causes and Consequences

The confluence of factors within the finance industry and the broader economy led to the onset of the 2008 financial crisis. However, the primary cause of this crisis can be attributed to the deregulation of the financial industry, which allowed banks to participate in hedge fund trading involving derivatives. This deregulation enabled banks to demand an increased number of mortgages to support the profitable sale of these derivatives. To cater to subprime borrowers, the banks introduced interest-only loans that appeared to be affordable.

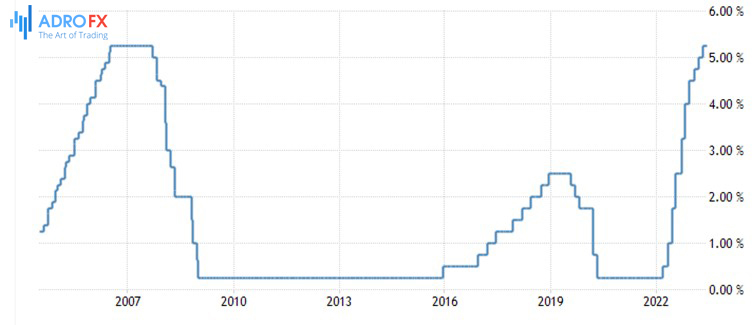

The situation worsened when, in 2004, the Federal Reserve decided to raise the fed funds rate just as the interest rates on these newly introduced mortgages were resetting. As a consequence, housing prices began to decline in 2007 due to an oversupply relative to demand. This decline in housing prices trapped homeowners who could neither afford their mortgage payments nor sell their houses. Furthermore, when the values of the derivatives plummeted, banks became hesitant to lend to each other. This created a severe financial crisis, ultimately leading to the Great Recession.

Deregulation

In 1999, the Gramm-Leach-Bliley Act, also known as the Financial Services Modernization Act, was passed, effectively overturning the Glass-Steagall Act of 1933. This act deregulated the financial industry and allowed banks to use deposits for investment in derivatives. Bank lobbyists argued that this change was necessary to compete with foreign firms and emphasized that they would only invest in low-risk securities to protect their customers' interests.

The following year, the Commodity Futures Modernization Act was enacted, granting exemptions to credit default swaps and other derivatives from regulatory oversight. This federal legislation superseded previous state laws that restricted speculative activities. Notably, it specifically excluded regulations on trading energy derivatives.

The driving force behind the passage of both acts was Senator Phil Gramm from Texas, who chaired the Senate Committee on Banking, Housing, and Urban Affairs. It is important to note that Senator Gramm received input from lobbyists representing Enron, an energy company. Additionally, Senator Gramm's wife had previously served as the Chairwoman of the Commodities Future Trading Commission and was a member of Enron's board. Enron, a major contributor to Senator Gramm's political campaigns, sought to participate in derivatives trading through its online futures exchanges. Enron argued that foreign derivatives exchanges were granting unfair competitive advantages to overseas firms.

Furthermore, influential figures like Federal Reserve Chairman Alan Greenspan and former Treasury Secretary Larry Summers actively advocated for the passage of these acts.

Securitization

Securitization involved a complex process that began with the sale of various financial instruments, including mortgage-backed securities (MBS), collateralized debt obligations (CDOs), and derivatives by hedge funds and other entities. Mortgage-backed securities represented the value of underlying mortgages used as collateral. Banks would sell these mortgages on the secondary market after individuals obtained them from the bank.

Hedge funds would then bundle similar mortgages together, using computer models to assess the value of the mortgage bundle based on factors like monthly payments, total debt, repayment likelihood, and future home prices. These mortgage-backed securities were subsequently sold to investors.

Once the bank sold the mortgage, it could use the funds received to issue new loans. While the bank still collected payments from borrowers, these payments were forwarded to the hedge fund, which then distributed them to its investors. Throughout this process, various parties involved took a share of the profits, making securitization an attractive strategy for both banks and hedge funds due to its perceived low risk.

Investors, however, assumed the risk of default. To mitigate their concerns, insurance known as credit default swaps (CDS) were available. Companies like American International Group (AIG) sold these CDS, providing a safety net for investors. This insurance coverage encouraged investors to eagerly invest in these derivatives. Over time, ownership of these securities expanded to include pension funds, large banks, hedge funds, and even individual investors. Notable owners of these derivatives included Bear Stearns, Citibank, and Lehman Brothers.

The profitability of derivatives backed by real estate and insurance was significant. As demand for these derivatives grew, banks had to increase the number of mortgages to support the creation of these securities. To meet this demand, banks and mortgage brokers relaxed lending standards and offered home loans to a wide range of borrowers.

The Fed Raised Rates on Subprime Borrowers

Following the 2001 recession, banks, which had been heavily impacted by the economic downturn, welcomed the introduction of new derivative products. In response to the recession, Federal Reserve Chairman Alan Greenspan lowered the Fed funds rate to 1.75% in December 2001. This rate was further reduced to 1.25% in November 2002.

The rate reductions also led to lower interest rates on adjustable-rate mortgages, making the payments on these mortgages more affordable. These mortgages were tied to short-term Treasury bill yields, which are influenced by the Fed funds rate. However, the decrease in interest rates affected banks' incomes, as their revenues heavily relied on loan interest rates.

The availability of interest-only loans became appealing to many individuals who couldn't afford conventional mortgages. As a result, the proportion of subprime mortgages surged, more than doubling to reach 14% by 2007. The creation of mortgage-backed securities and the functioning of the secondary market played a role in ending the 2001 recession.

However, this situation also contributed to an asset bubble in the real estate market by 2005. The high demand for mortgages drove up housing demand, leading homebuilders to meet this demand. Many people took advantage of the low-interest loans and purchased homes as investments, with the intention of selling them as prices continued to rise.

A significant number of borrowers with adjustable-rate loans were unaware that their rates would reset after three to five years. In 2004, the Federal Reserve began raising interest rates, reaching 2.25% by the end of the year. Subsequently, by the end of 2005, it had risen to 4.25%. Finally, by June 2006, the rate had climbed to 5.25%. Homeowners found themselves burdened with payments they couldn't afford, as these interest rates increased at a faster pace compared to previous fed funds rate adjustments.

By 2005, homebuilders had met the high housing demand, leading to an oversupply of homes. Consequently, housing prices began to decline. From their peak in April 2006 to their lowest point in March 2011, home prices experienced a significant drop of 33%.

The decline in home prices had a profound impact on mortgage holders, as they couldn't sell their homes for a value that covered their outstanding loan amounts. Additionally, the Federal Reserve's rate increase worsened the situation for new homeowners, who struggled to afford rising mortgage payments. This bursting of the housing market bubble became evident and triggered a banking crisis in 2007, which eventually spread to Wall Street in 2008.

These events set off a cascading effect, with the collapse of the housing market serving as a catalyst for the broader financial crisis that unfolded in the following years.

Consequences of the 2008 Financial Crisis

The 2008 financial crisis had far-reaching consequences that impacted economies, financial markets, and individuals around the world. Some of the significant consequences of the crisis include:

Global Recession

The financial crisis triggered a severe global recession, as it originated in the United States but quickly spread to other parts of the world. Many countries experienced negative GDP growth, high unemployment rates, and a decline in business activity.

Bank Failures and Bailouts

Several major banks and financial institutions faced insolvency or collapsed during the crisis. Lehman Brothers, one of the largest investment banks, filed for bankruptcy, leading to a loss of confidence in the financial system. Governments intervened to prevent the complete collapse of the banking sector, providing bailouts and financial support to stabilize the industry.

Housing Market Crash

The crisis was primarily caused by the bursting of the US housing bubble, with a subsequent decline in housing prices and an increase in mortgage defaults. Many homeowners found themselves with negative equity (owing more than their homes were worth), leading to a wave of foreclosures and distressed properties.

Unemployment and Job Losses

The financial crisis resulted in significant job losses across various sectors. As businesses faced financial difficulties and reduced consumer spending, they were forced to downsize, lay off workers, or shut down altogether. Unemployment rates soared, leading to hardship for many individuals and families.

Government Debt and Austerity Measures

Governments worldwide incurred substantial debt to finance the bailouts, stimulus packages, and social safety nets put in place to mitigate the crisis's impact. As a result, many countries faced increased levels of public debt, which led to subsequent austerity measures, such as spending cuts, tax increases, and reduced public services.

Stock Market Volatility

Stock markets experienced significant volatility during the crisis. Stock prices plummeted, causing investors to lose confidence and leading to a sharp decline in market capitalization. It took several years for markets to recover and regain stability.

Regulatory Reforms

The financial crisis exposed weaknesses and flaws in the regulatory frameworks governing the financial industry. Governments and regulatory bodies implemented various reforms to strengthen oversight, increase transparency, and prevent a similar crisis from happening again. Examples include the Dodd-Frank Act in the United States and the Basel III framework internationally.

Public Distrust and Loss of Confidence

The crisis eroded public trust in financial institutions, governments, and the overall economic system. People became disillusioned with the perceived greed, risk-taking, and lack of accountability demonstrated by some financial actors. Restoring confidence and rebuilding trust in the financial sector has been an ongoing challenge.

Long-Term Economic Impact

The 2008 financial crisis had long-term effects on economic growth. Many countries experienced a slower recovery, with prolonged periods of low growth and stagnant wages. The crisis also highlighted structural issues within economies, such as income inequality and disparities in wealth distribution.

Increased Focus on Financial Regulation

The crisis prompted a reevaluation of financial regulation and led to the implementation of stricter rules and oversight. Regulators placed a greater emphasis on risk management, capital requirements, and stress testing to ensure the stability of financial institutions and the overall system.

It is important to note that the consequences of the 2008 financial crisis varied across countries and regions, depending on factors such as their exposure to the crisis, economic policies, and the resilience of their financial systems.

Conclusion

In conclusion, the 2008 financial crisis was a complex event with multiple causes and far-reaching consequences. Deregulation within the financial industry, particularly the repeal of the Glass-Steagall Act and the subsequent Commodity Futures Modernization Act, played a significant role in allowing banks to engage in risky trading practices and the creation of mortgage-backed securities. The proliferation of these securities, coupled with a housing market bubble and the Federal Reserve's raising of interest rates, led to the bursting of the bubble and a subsequent collapse in the housing market. The crisis had profound effects globally, including a severe recession, bank failures, a housing market crash, high unemployment rates, and increased government debt. It also exposed flaws in financial regulation, leading to regulatory reforms and a focus on strengthening oversight and transparency. Public trust in financial institutions and the economy suffered, and long-term economic impacts, such as slow growth and income inequality, continue to be felt. The crisis serves as a reminder of the importance of prudent regulation, risk management, and accountability within the financial sector to prevent future crises.

About AdroFx

Established in 2018, AdroFx is known for its high technology and its ability to deliver high-quality brokerage services in more than 200 countries around the world. AdroFx makes every effort to keep its customers satisfied and to meet all the trading needs of any trader. With the five types of trading accounts, we have all it takes to fit any traders` needs and styles. The company provides access to 115+ trading instruments, including currencies, metals, stocks, and cryptocurrencies, which make it possible to make the most out of trading on the financial markets. Considering all the above, AdroFx is the perfect variant for anyone who doesn't settle for less than the best.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates