Moody's Downgrades Spark Selloff, Chinese Deflation Concerns, and Disney's Revenue Anticipation | Daily Market Analysis

Key events:

- USA - Crude Oil Inventories

- China - CPI (MoM) (Jul)

- China - PPI (YoY) (Jul)

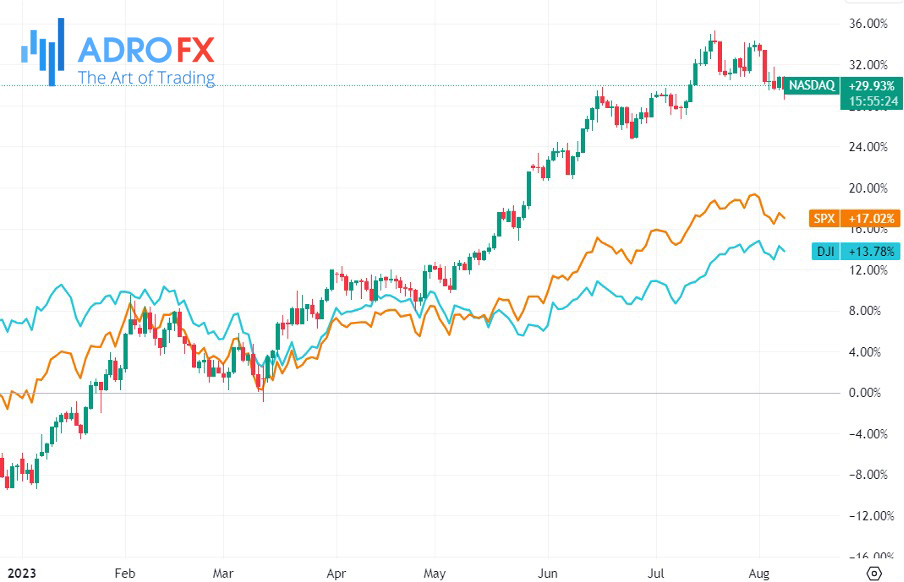

On Tuesday, all three major stock market indicators on Wall Street concluded with losses, as a widespread selloff was prompted by credit rating agency Moody's (NYSE: MCO) downgrading several financial institutions. This event rekindled concerns regarding the well-being of both US banks and the overall economy.

Following five months of gains that brought the S&P 500 and Nasdaq Composite benchmarks to within 5% of their all-time highs, August has witnessed a total of six sessions, five of which ended in losses. During this month, the S&P has fallen by 2%, while the Nasdaq has experienced a decline of 3.2%.

The descent on Tuesday was set in motion by the agency's decision to lower the ratings of ten smaller to medium-sized lenders by a single level. Additionally, it placed six banking behemoths, including Bank of New York Mellon (NYSE: BK), US Bancorp, State Street (NYSE: STT), and Truist Financial (NYSE: TFC), under review for potential future downgrades.

The release of disappointing China trade figures for July triggered a significant sell-off in both European and US markets. This reinforced worries that the Chinese economy is facing difficulties, challenging the optimism that the slowdown observed in the second quarter was merely an isolated occurrence.

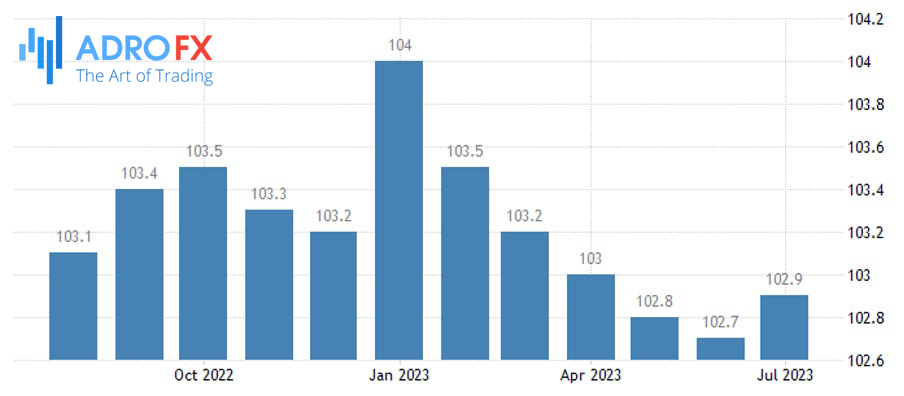

This morning, the headline Consumer Price Index (CPI) inflation in China followed the Producer Price Index (PPI) measure and entered a state of outright deflation for the first time in 28 months.

This development has intensified concerns that despite assurances of further stimulus actions, Chinese authorities might be encountering constraints in terms of the type of stimulus they can effectively employ to stimulate domestic demand.

The CPI inflation figure declined from 0.2% in June to -0.3% in July, while the PPI registered at -4.4%. Remarkably, this marks the tenth consecutive month of negative prices in the PPI.

The issue of Chinese deflation has been a significant factor influencing recent tightening measures from central banks such as the Federal Reserve, the European Central Bank (ECB), and the Bank of England. The presence of a clear deflationary force originating from Asia raises questions about the potential number of future rate hikes in the coming months. Moreover, there is growing concern about the tipping point at which the risk of excessive tightening becomes a pressing issue.

The European banking sector is currently grappling with the aftermath of Italy's unexpected approval of a windfall tax of 40%. However, authorities clarified in a statement released on Tuesday that this newly introduced tax would not exceed 0.1% of a lender's total assets. European markets are now alert for any similar actions taken by other countries.

Attention is now shifting towards the upcoming US inflation report, following mostly cautious remarks from several Federal Reserve officials during this week. Given that the next policy meeting is not slated until September, the US central bank still has ample time to closely monitor crucial pricing data.

During the Asian morning session, the strength of the dollar slightly moderated, having experienced a boost from safe-haven purchases stemming from discouraging trade data from China on Tuesday.

On Wednesday, gold prices stabilized close to their one-month lows due to deteriorating market sentiment and the anticipation of additional Federal Reserve interest rate hikes. This situation prompted investors to shift towards the dollar.

The prevailing strength of the dollar exerted downward pressure on the wider metal markets. Investors were in a state of anticipation for further economic indicators from the US.

Given the decline in global risk sentiment, investors remained inclined towards the greenback as their preferred safe haven in anticipation of the upcoming inflation reading.

In the midst of yet another busy week filled with corporate earnings reports, an extra dose of excitement could be on the horizon courtesy of the Magic Kingdoms. Walt Disney (NYSE: DIS) Co is anticipated to unveil an increase in revenue when it reports on Wednesday.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates