Markets React to Economic Concerns and Apple's China Challenge While Awaiting US Inflation Data | Daily Market Analysis

Key events:

- UK - BoE MPC Member Pill Speaks

- USA - 3-Year Note Auction

On Friday, the S&P 500 managed to eke out a slight gain, although it ended well below its peak for the session. Unfortunately, all three of Wall Street's major indices posted weekly declines as investors grappled with concerns about interest rates and anxiously awaited forthcoming US inflation data.

One of the key concerns among investors has been the surge in oil prices, and their apprehension has only deepened ahead of the release of the Consumer Price Index (CPI) for August, scheduled for September 13. This report is highly anticipated as it is expected to provide insights into the Federal Reserve's potential actions regarding interest rates.

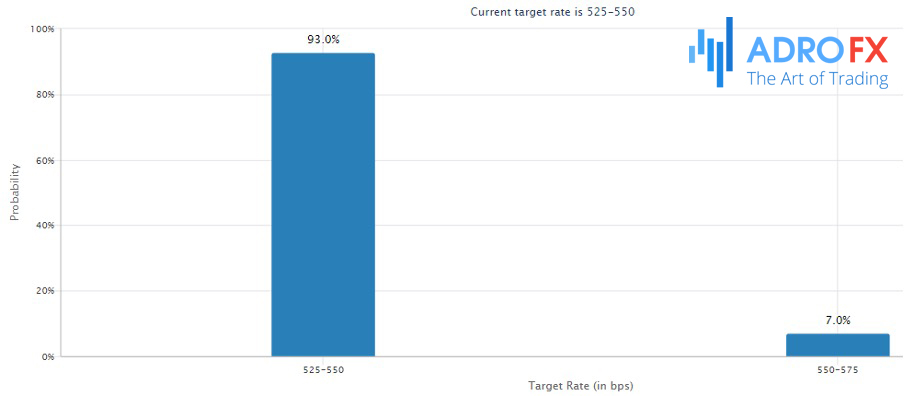

Currently, traders are placing bets with a roughly 93% likelihood that the Federal Reserve will maintain its current interest rate levels following the conclusion of its next meeting on September 20, according to CME Group's FedWatch Tool.

While yields on the benchmark US 10-year Treasury notes saw a decline, the uptick in US 2-year Treasury yields on Friday seemed to exert pressure on the stock market.

Apple Inc (NASDAQ: AAPL) appears to be unfazed by concerns regarding weakening demand in China, even as reports suggest that China has expanded its ban on iPhones to include local government workers and state-owned companies.

This development comes shortly after news indicated that Beijing had prohibited central government employees from using foreign devices, including iPhones, citing national security concerns.

However, some voices on Wall Street argue that the selloff in Apple shares driven by these China-related issues may be exaggerated. Wedbush, for instance, commented that "Any China government agency iPhone ban is way overblown." They pointed out that the China government agency's ban would impact "less than 500,000 iPhones out of roughly 45 million" expected to be sold in China over the next year.

In the currency markets, the Japanese yen saw a significant jump on Monday, driven by remarks from Bank of Japan (BOJ) Governor Kazuo Ueda that raised hopes of a shift away from negative interest rates in Japan. This surge in the yen was in contrast to a weakening US dollar, which was influenced by anticipation surrounding the upcoming US inflation data.

The yen strengthened over 1% to reach a one-week high of 145.99 per dollar following Ueda's comments. He mentioned that the BOJ could consider ending its negative interest rate policy when it gets closer to achieving its 2% inflation target, possibly by the end of the year.

The euro also gained ground, rising by 0.36% to $1.0738, breaking an eight-week losing streak. Meanwhile, the dollar index, which had seen eight consecutive weeks of gains, fell by 0.31% to 104.53.

In the European stock markets, there were modest expectations for a slight opening gain. Investors were exercising caution as they awaited the European Central Bank's policy-setting meeting scheduled later in the week.

Futures contracts for the DAX in Germany traded 0.3% higher, while those for the CAC 40 in France climbed 0.3%, and the FTSE 100 in the UK rose 0.4%. The ECB meeting later in the week was generating uncertainty among investors, given elevated price pressures alongside signs of economic slowdown.

Italy was anticipated to release data illustrating this economic downturn, with industrial production in the eurozone's third-largest economy expected to have fallen by 0.3% on a monthly basis in July, resulting in an annual drop of 1.7%.

Recent data showed that the eurozone's GDP grew by just 0.1% in the second quarter compared to the previous three months, while consumer prices in Germany, the largest economy in the eurozone, rose by an annualized rate of 6.1% in August, well above the central bank's medium-term 2% target.

The ECB has raised interest rates at its last nine meetings, and policymakers are now debating whether to increase the deposit rate to 4% or take a pause. The challenge they face is deciding whether further tightening is necessary, with September appearing to be the last opportunity for such a move.

Investors will also closely monitor economic developments in the United States this week, as key US inflation data is scheduled to be released. The latest Consumer Price Index (CPI) is set to be unveiled on Wednesday, followed by the Producer Price Index (PPI) on Thursday.

These data releases follow a series of economic reports from the previous week that exceeded expectations, reigniting concerns that the US Federal Reserve might opt for a more substantial rate hike than initially anticipated.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates