Market Sentiment Remains Positive Amid Signs of Disinflation; US and UK Economic Indicators in Focus | Daily Market Analysis

tKey events:

- China - Industrial Production (YoY) (Jun)

- Eurozone - ECB President Lagarde Speaks

- Eurozone - ECB's Lane Speaks

- USA - NY Empire State Manufacturing Index (Jul)

On Friday, US stocks closed with a slight decline, but overall, investors remained optimistic amid indications that disinflation might be a more sustained trend. As investors pondered the potential effects on interest rates, stock markets, and the Federal Reserve's actions, the overall sentiment remained positive.

The market sentiment seemed to reflect growing confidence in the possibility of a soft landing for the economy. Yields experienced a significant decrease, especially towards the end of the week, and this decline is occurring for what many consider the "right" reasons. Investors are adjusting their estimates by removing inflation premiums, rather than assuming the Federal Reserve will cut rates in response to inflationary pressures.

The unexpected decline in US CPI triggered a market reaction, leading to a compression of US-EU front-end rate spreads, while the inversion in the US front-end rates deepened. However, as the drop in inflation provides relief and signals progress towards a soft landing for the economy, the Federal Reserve is likely to maintain its current stance and not make significant rate adjustments over the next 12 months. Consequently, the US Dollar may not experience a significant freefall in value.

When looking at the rates outlook, there isn't a substantial divergence for a significant portion of the broad Dollar index. Many policymakers across various emerging markets (EM) are already responding to the lower inflation environment. The Euro area is expected to follow suit and not be far behind in terms of rate adjustments.

While US rates were primarily influenced by domestic factors, Euro area rates began responding towards the end of the week, suggesting that developments in the US economy and inflation relief are starting to impact global rate trends, including the Eurozone.

The second-quarter earnings season is about to kick off, and Tesla (NASDAQ: TSLA) will be the first of the massive growth and technology names, which have been the driving force of the US stock market this year, to report its results, scheduled for Wednesday.

Tesla is part of the group of seven colossal stocks, including Apple (NASDAQ: AAPL), Microsoft (NASDAQ: MSFT), Alphabet (NASDAQ: GOOGL), Amazon (NASDAQ: AMZN), Nvidia (NASDAQ: NVDA), and Meta Platforms (NASDAQ: META), collectively known as the "Magnificent Seven" among investors. These megacap companies have witnessed remarkable share price surges ranging from 40% to over 200% so far this year, contributing significantly to the overall rally of the S&P 500.

While there are signs that the market rally is extending to other sectors, it's important to note that the substantial gains have been accompanied by high earnings expectations. If Tesla or any of the other megacap companies fail to meet these expectations during this quarter's earnings reports, it could result in a severe impact on equity indices.

Alongside Tesla's earnings report, numerous other major companies are also set to disclose their results in the upcoming week. The banking sector's earnings season continues, with Bank of America (NYSE: BAC) announcing its results on Tuesday and Goldman Sachs (NYSE: GS) on Wednesday.

On Tuesday, the US retail sales data for June is anticipated to show a 0.5% increase, driven by a recovery in auto sales and higher gasoline station sales. This indicates that consumer demand remains resilient despite some challenges.

Investors will also be keeping an eye on reports concerning regional manufacturing activity, which is expected to remain sluggish. Additionally, the weekly data on initial jobless claims will provide insights into the current state of the job market.

On Wednesday, the UK will release its June inflation data, a critical factor that will likely influence the size of the Bank of England's next interest rate hike.

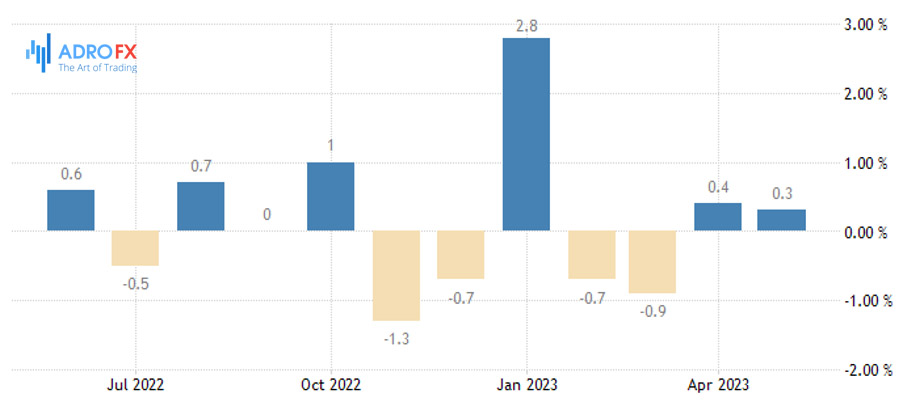

The headline consumer price index is expected to ease to 8.2% year-over-year, down from 8.7% in May, primarily due to a decline in food and fuel prices. Core inflation is also anticipated to decrease slightly, but the services component is expected to remain steady at a post-COVID high of 7.4%.

In the June meeting minutes, the Bank of England stated that further tightening would be necessary if the economy showed signs of persistent inflationary pressures, particularly in the services consumer price index (CPI).

As a result, the August meeting of the Bank of England could be a close call. If there is an uptick in services CPI, it would likely solidify expectations for another 50-basis point rate hike. Conversely, a lower reading would probably tilt the scales in favor of a smaller 25 basis points increase. The inflation data will play a significant role in shaping the central bank's decision on future interest rate adjustments.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates