Market Sentiment Remains Cautious Despite Tesla Surge and S&P 500's Winning Streak | Daily Market Analysis

Key events:

- UK - BoE MPC Member Mann

- USA - Federal Budget Balance (May)

On Friday, the S&P 500 experienced a rise in its closing value, although it fell short of the session's peak levels. The market failed to rally extensively despite a notable surge in Tesla (NASDAQ: TSLA) shares, as investors remained cautious ahead of the Federal Reserve's policy meeting and upcoming inflation data the following week.

Tesla Inc shares recorded a 4.06% increase, marking their lengthiest winning streak since January 2021. This surge was attributed to the announcement that General Motors Co (NYSE: GM) had agreed to utilize Tesla's Supercharger network. Consequently, General Motors' shares also saw a rise of 1.06%.

The S&P 500 index recorded a gain of 4.93 points, equivalent to 0.11%, closing at 4,298.86. This week's performance contributed to an overall advance of 0.38% and marked the index's fourth consecutive week of gains, the longest winning streak since the period between July and August 2022. The Nasdaq Composite also experienced its seventh consecutive week of gains, with an increase of 20.62 points or 0.16%, reaching a closing value of 13,259.14 for the day and a weekly gain of 0.13%.

The ongoing rally in mega-cap stocks, a better-than-expected earnings season, and the perception that the Federal Reserve was nearing the end of its rate-hiking cycle have provided support to Wall Street throughout the year. These factors have helped alleviate concerns surrounding an impending recession and persistent inflationary pressures.

The Bank of Japan (BoJ) holds the potential to bring about the only significant policy surprise this week. The USD/JPY currency pair has been trading within the range of 139-140, leading to speculation regarding potential foreign exchange (FX) intervention and a potential policy shift by the BoJ in response.

However, it is unlikely that intervention will occur based on the previous stance taken by the BoJ, which set a line in the sand at around 143 levels. The central bank conducted rate checks last September and carried out interventions at that threshold. Nonetheless, the BoJ's new guidance allows for flexible adjustments to yield curve control (YCC) in response to factors such as an excessively weak yen or stronger-than-expected inflation.

Given the current movement of USD/JPY, which has risen close to 140 from around 134 prior to the April Monetary Policy Meeting (MPM), market participants will pay close attention to Governor Ueda's comments on this matter. His statements regarding the yen's strength and inflationary trends are likely to attract significant scrutiny and interest.

Meanwhile, the CBOE Volatility Index, often referred to as the fear gauge of Wall Street, initially dropped to its lowest level since February 2020 but later recovered some of its losses.

In Asian trade, the US dollar strengthened, as both the dollar index and dollar index futures recorded a 0.1% increase.

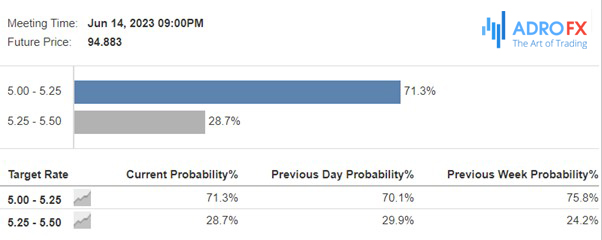

This week's economic calendar features several significant events, with Wednesday's Federal Open Market Committee (FOMC) meeting taking the spotlight. As the primary "market maker" globally, this meeting will provide crucial insights into inflation, consumer spending, and factory sector activity. Following a series of ten consecutive rate hikes in previous FOMC meetings, the general expectation is for the Fed to maintain a steady stance this Wednesday, keeping the Fed funds rate unchanged at 5.125%.

However, the market will closely scrutinize the meeting statement, the Summary of Economic Projections (SEP), and Chair Powell's press conference, which are expected to lean towards a more hawkish tone. This suggests that further policy tightening may be necessary, potentially as early as the July 26 meeting. Consequently, a hawkish hold is the favored outcome based on market expectations.

The dot plot, a graphical representation of the Fed members' interest rate projections, is also anticipated to indicate the potential need for an additional rate hike in order to achieve a "sufficiently restrictive" policy. This outlook is influenced by robust economic data, accommodative financial conditions, and the desire to prevent an early shift in rate-cut expectations. As this scenario has already been factored into market forecasts, the impact on equities should be minimal unless Chair Powell delivers an excessively hawkish message during the press conference.

In terms of economic data, the Consumer Price Index (CPI) is expected to decrease to 4.1% from the previous month's reading of 4.9%.

The European Central Bank (ECB) is anticipated to follow through on its previous commitment to tightening measures during Thursday's meeting. A 25 basis points rate hike is already factored into market expectations. ECB President Christine Lagarde, in the previous meeting, mentioned the potential for further action in June, July, or even September to ensure a prompt return of inflation to the target of 2%. However, she may be cautious during the press conference in providing forward guidance.

Lagarde is likely to emphasize that the ECB's complete cessation of reinvestments under the Asset Purchase Programme (APP) will take effect the following week. This decision will result in the withdrawal of an additional €160 billion of liquidity from the market over the next 12 months.

Additionally, there are several other data releases scheduled, including the Producer Price Index (PPI), retail sales figures, Philadelphia Fed Manufacturing Business Outlook Survey, retail inventories, and reports on Michigan consumer sentiment and expectations. Moreover, market participants will closely monitor speeches from James Bullard and Christopher Waller, members of the Federal Reserve, for any insights or indications of future monetary policy decisions.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates