Investors Shake Off Tariff Fears as Markets Close the Week on a High Note | Weekly Market Analysis

Key events this week:

Wednesday, April 16, 2025

- China - GDP (YoY) (Q1)

- UK - CPI (YoY) (Mar)

- Eurozone - CPI (YoY) (Mar)

- USA - Core Retail Sales (MoM) (Mar)

- USA - Retail Sales (MoM) (Mar)

- Canada - BoC Interest Rate Decision

- USA - Crude Oil Inventories

- USA - Fed Chair Powell Speaks

Thursday, April 17, 2025

- USA - Initial Jobless Claims

- USA - Philadelphia Fed Manufacturing Index (Apr)

- Eurozone - ECB Press Conference

- Eurozone - Deposit Facility Rate (Apr)

- Eurozone - ECB Interest Rate Decision (Apr)

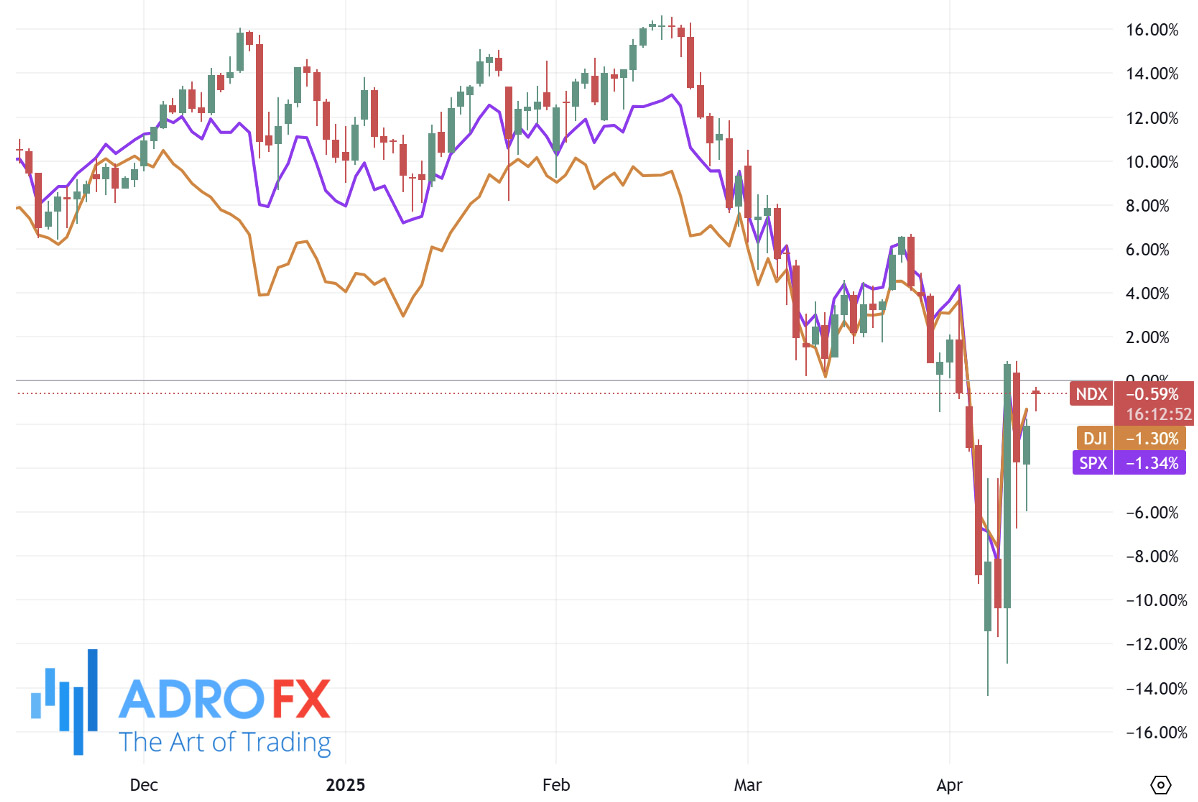

US markets wrapped up a turbulent week on a positive note Friday, with the S&P 500 posting solid gains despite escalating tensions between the US and China and renewed concerns surrounding the American consumer and inflation pressures. Investors seemed willing to look past the growing trade discord and weak consumer sentiment, choosing instead to focus on corporate earnings and easing inflation fears.

The S&P 500 ended the session with a notable advance, accompanied by a 619-point surge in the Dow Jones Industrial Average, marking a 1.6% climb. The tech-heavy NASDAQ outperformed its peers, rising 2.1% as investors rotated back into growth stocks after a recent selloff. Despite volatility throughout the week, all three indices closed higher, suggesting a resilient appetite for risk among market participants.

However, not everything was smooth on the macroeconomic front. The University of Michigan’s preliminary consumer sentiment index for April revealed a sharp 11% drop from the previous month, falling to 50.8 - its second-lowest reading since records began. The slide was attributed to growing unease among households about the economic implications of US tariffs, which many perceive as threatening their financial stability and job security.

At the same time, expectations for inflation saw a sharp increase. Consumers surveyed by the University of Michigan projected long-term price growth to exceed 4%, citing uncertainty around economic policy changes. The upward revision in the inflation outlook has added to investor anxiety, though market pricing still leans toward future policy easing from the Fed rather than tightening.

Amid these economic concerns, Federal Reserve commentary provided a touch of reassurance. Boston Fed President Susan Collins indicated the central bank stands ready to intervene if financial conditions deteriorate significantly, underscoring the Fed’s commitment to supporting markets in times of stress.

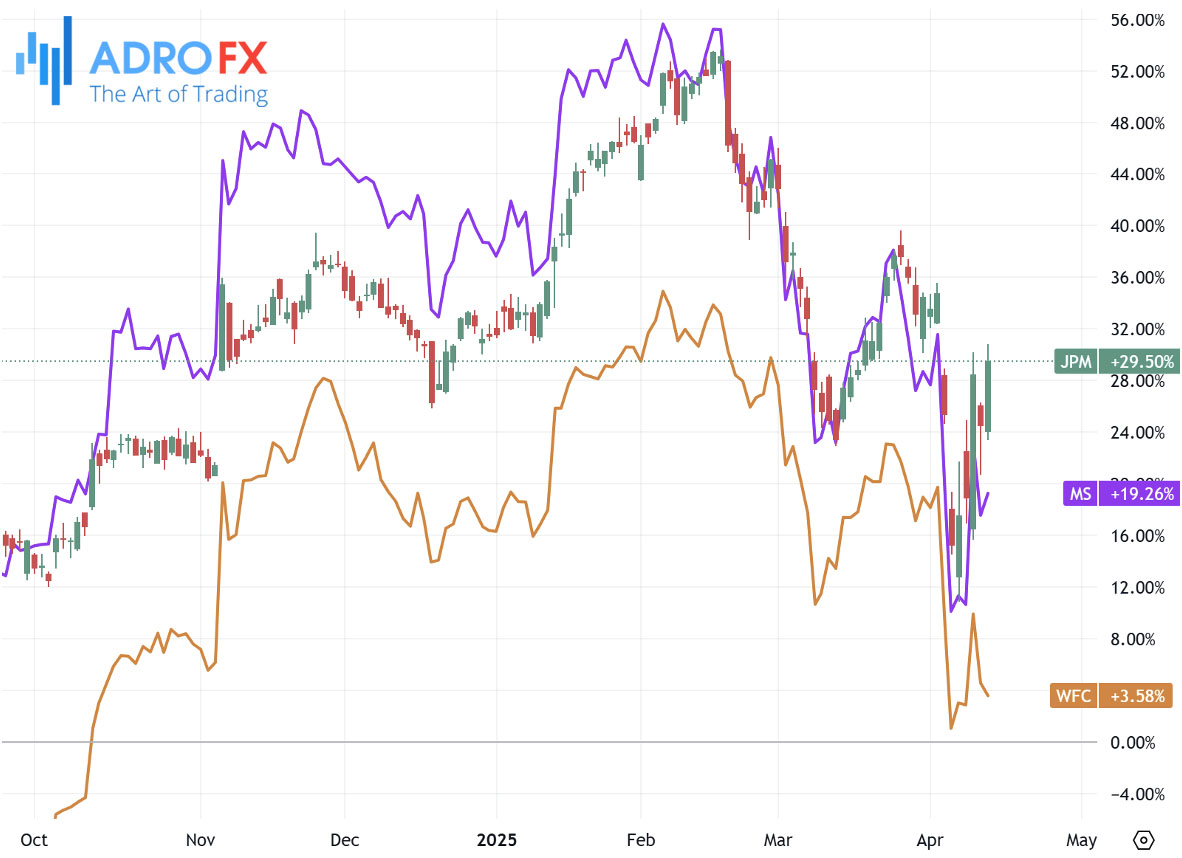

Meanwhile, the unofficial kickoff to earnings season saw several major US banks - JPMorgan Chase, Wells Fargo, and Morgan Stanley - beat analysts' expectations. Despite the upbeat results, executives from these institutions struck a cautious tone regarding the broader economic environment, pointing to headwinds from slowing growth and persistent inflation.

In the tech space, Apple rallied more than 4%, recovering ground lost in recent weeks as bargain hunters stepped in. Tesla, however, was mostly flat after the company temporarily halted Model S and Model X orders in China amid tariff-related disruptions, a move that raised questions about near-term sales performance in the world’s largest EV market.

Turning to commodities, gold entered a phase of bullish consolidation just shy of its all-time high near $3,230, touched earlier in the Asian session. Despite appearing overbought on the daily chart, the broader backdrop - characterized by global uncertainty and weakening currencies - suggests that gold’s upward trajectory may still have room to run.

The New Zealand Dollar extended its rally for a fourth consecutive session, trading near 0.5840 as sentiment turned more positive. Support came from President Trump’s announcement that planned tariff hikes on certain Chinese imports would be less aggressive than anticipated. In particular, items like semiconductors and electronics will remain subject to existing 20% duties, rather than the rumored 145%, easing pressure on regional trade partners like New Zealand.

Also boosting NZD was a stronger-than-expected trade report out of China. March trade data showed the country’s surplus ballooning to CNY 736.72 billion from February’s CNY 122 billion. In dollar terms, the figure came in at $102.6 billion, comfortably topping expectations. Exports surged 13.5% year-on-year, while imports contracted at a slower pace than the previous month, signaling a degree of resilience in the Chinese economy.

China’s customs officials acknowledged the difficult external environment but expressed confidence in the nation’s ability to maintain growth momentum. Authorities reiterated their commitment to countering US trade actions with appropriate policy responses while continuing to defend national economic interests.

The US Dollar Index declined for the third session in a row, sliding toward 99.50 and approaching a three-year low. The Greenback has been pressured by soft economic data and dovish signals from Fed officials, who are increasingly seen as likely to lower rates multiple times by year-end.

The Japanese Yen maintained its positive tone, trading near highs not seen since late September 2024. Ongoing trade tensions between the US and China, coupled with speculation that the Bank of Japan may continue its tightening cycle into 2025, have increased the appeal of the JPY as a safe-haven currency. This outlook sharply contrasts with market expectations for aggressive rate cuts by the Federal Reserve, further tilting the balance in favor of the Yen.

The Australian Dollar also benefited from the broader shift in sentiment, gaining ground against the Greenback. Stronger commodity prices lent support to the AUD, though lingering uncertainty over US-China relations continued to weigh on its longer-term prospects. Given Australia’s dependence on China for trade, developments in Beijing’s negotiations with Washington remain a crucial variable.

The Canadian Dollar lost ground for the fourth session running, with the USD/CAD pair hovering around 1.3860. Weakness in the US Dollar contributed to the movement, but subdued oil prices limited the CAD’s upside potential. West Texas Intermediate crude hovered near $60.70 per barrel as markets weighed the potential impact of renewed trade tensions on global demand. Canada, being a major oil exporter to the US, is particularly sensitive to shifts in energy prices.

The euro pulled back slightly during the Asian session, with EUR/USD hovering around 1.1360 after two sessions of gains. Traders reacted to the European Union’s decision to suspend planned retaliatory tariffs for 90 days - a gesture aimed at de-escalating transatlantic trade friction. This followed a similar move by the US, signaling a mutual willingness to re-engage in constructive dialogue.

On the political front, German Chancellor-in-waiting Friedrich Merz voiced concern over Trump’s economic strategy, warning that such policies could bring forward the next financial crisis. In a weekend interview, he advocated for a comprehensive new trade deal with the US, suggesting that eliminating tariffs on both sides would benefit the global economy.

Looking ahead, traders will keep a close eye on remarks from Federal Reserve Chair Jerome Powell and other key policymakers. With US retail sales data also set for release midweek, the market will be hunting for clues on whether inflationary pressures are easing and how that might shape the Fed’s path forward. These developments could be pivotal for the trajectory of the US dollar and gold prices as the week unfolds.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates