Global Stocks Navigate Peaks, Central Banks Signal Policy Shifts | Daily Market Analysis

Key events:

- USA - Existing Home Sales

- USA - Existing Home Sales (Oct)

- USA - FOMC Meeting Minutes

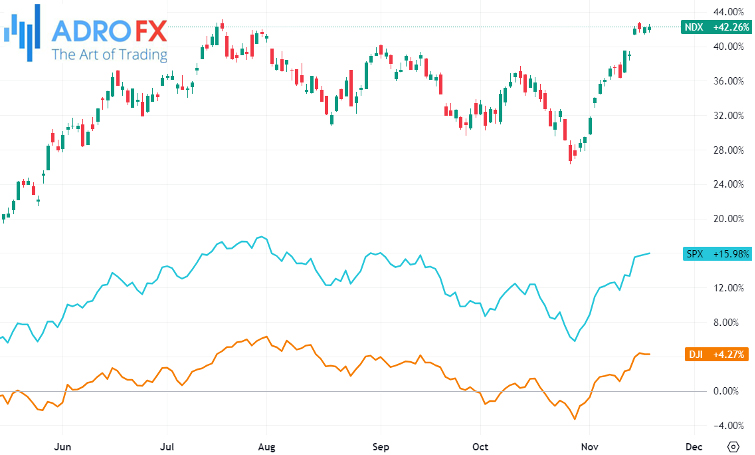

Global stocks held steady near two-month highs on Friday, and Treasury yields briefly touched two-month lows as investors maintained the belief that US interest rates have reached their peak and could potentially decrease next year.

However, a reality check occurred when Federal Reserve Bank of Boston President Susan Collins stated on Friday that while there is growing evidence of easing inflation, she was not ready to dismiss the possibility of additional rate hikes if deemed necessary.

This tempered the enthusiasm on Wall Street, resulting in the Dow Jones Industrial Average and the Nasdaq Composite finishing flat, while the S&P 500 posted a modest gain of just 0.13%.

On Monday, the dollar continued its decline, reaching a two-month low and extending the downtrend observed throughout the previous week. Traders reinforced their belief that US interest rates have peaked, shifting their focus to when the Federal Reserve might initiate rate cuts.

During Asian trade, the dollar index hit a bottom of 103.64, marking its weakest level since September 1. This extended its nearly 2% decline from the previous week, representing the sharpest weekly fall since July.

The market sentiment has shifted, reflecting reduced expectations of further rate hikes by the Federal Reserve. This shift followed a series of weaker-than-expected US economic indicators, particularly a below-estimate inflation reading.

Attention is now directed towards when the first rate cuts might occur, with futures indicating a 30% chance that the Fed could initiate rate reductions as early as next March.

Conversely, in response to the weakening dollar, the euro saw an increase, reaching an over two-month high of $1.0924. This surge occurred ahead of the release of flash PMI readings in the eurozone later in the week.

The weakening dollar contributed to a notable strengthening of the yen, trading below 150 per dollar.

US Treasury yields continued their sharp decline since the beginning of November, with the benchmark 10-year note yield briefly touching a two-month low. Later in the day, the 10-year note yield remained relatively unchanged at 4.439%, compared to 4.445% late on Thursday, while the two-year note rose by 6.1 basis points to yield 4.9025%, up from 4.842%.

The yield spread between two- and 10-year Treasury notes widened, signaling expectations of a slowing economy. The inversion of the curve reached around -46.0 basis points on Friday, a deepening from -38 basis points the previous day, hovering near its lowest level since early October.

In response to rate expectations, two-year bond yields in Germany and Britain reached their lowest levels since June. Money markets are now pricing in approximately 100 basis points worth of rate cuts in both the United States and the euro area.

In the upcoming holiday-shortened week, investors are eagerly anticipating insights into the future trajectory of interest rates as the Federal Reserve releases the minutes of its Oct. 31-Nov. 1 meeting on Tuesday. Recent signs of cooling inflation have raised hopes that the central bank may have concluded its rate hikes, prompting investors to scrutinize the minutes for indications of policymakers' inclinations.

Vice Chair for Supervision Michael Barr conveyed his view that the Federal Reserve has either reached or is in close proximity to the peak of interest rate hikes. However, San Francisco Fed Chief Mary Daly and Boston Fed President Susan Collins stressed the importance of gathering additional evidence indicating a cooling trend in inflation.

Upcoming economic data includes the release of figures on existing home sales on Tuesday, followed by weekly government reports on initial jobless claims and October data on durable goods orders a day later. US retailers are preparing for the kickoff of Black Friday, marking the crucial start to the holiday shopping season. Questions linger about the resilience of the consumer-driven US economy in light of elevated interest rates and ongoing inflation.

Recent data from the past week unveiled a slight decline in US retail sales for October, hinting at a potential slowdown in demand. Retailers, including Walmart, have issued warnings that this holiday season may not be as robust as previous years due to cautious consumer spending.

In the Eurozone, purchasing manager indices for November are set to be published on Thursday, with economists not anticipating a significant uptick in activity. Additionally, data on consumer confidence is due on Wednesday, and the highly watched German Ifo business climate index is scheduled for release on Friday.

The European Central Bank (ECB) will issue its latest financial stability review on Wednesday, followed by the release of the minutes of its October policy meeting a day later. ECB President Christine Lagarde is expected to make appearances in Berlin on Tuesday and in Frankfurt on Friday, accompanied by several other ECB officials making appearances throughout the week.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates