Wall Street Climbs to Record Highs as Rate Cut Bets Strengthen and Global Currencies React | Weekly Market Analysis

Key events this week:

Monday, August 25, 2025

- USA - New Home Sales (Jul)

Tuesday, August 26, 2025

- USA - Durable Goods Orders (MoM) (Jul)

- USA - CB Consumer Confidence (Aug)

Wednesday, August 27, 2025

- USA - Crude Oil Inventories

Thursday, August 28, 2025

- USA - GDP (QoQ) (Q2)

- USA - Initial Jobless Claims

Friday, August 29, 2025

- USA - Core PCE Price Index (MoM) (Jul)

- USA - Core PCE Price Index (YoY) (Jul)

- USA - Chicago PMI (Aug)

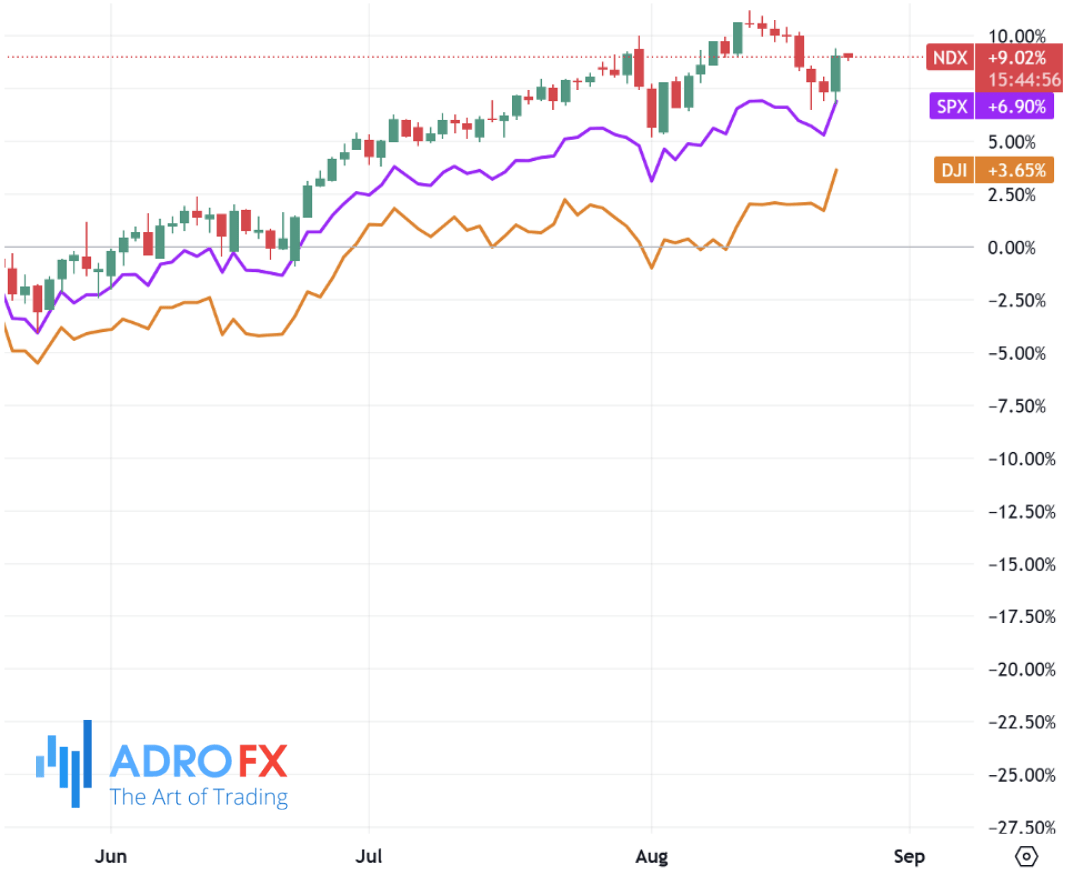

US equities closed last week on a powerful note, with the Dow Jones Industrial Average surging to an all-time high as fresh optimism over a potential September interest rate cut from the Federal Reserve reignited enthusiasm for stocks. Treasury yields fell sharply after Fed Chair Jerome Powell signaled the central bank was prepared to ease monetary policy as soon as next month if economic conditions warranted. Investors responded with a wave of buying, particularly in the technology sector, driving the major indices to impressive gains.

By Friday’s close, the Dow had jumped 846 points, or 1.9%, to a record level of 45,631.74. The S&P 500 followed with a gain of 1.6%, while the tech-heavy Nasdaq Composite surged 2%, as investors rushed back into growth names on expectations that lower rates could provide a meaningful tailwind.

The second-quarter earnings season also added fuel to the rally, with results coming in far stronger than Wall Street analysts had predicted earlier in the year. UBS boosted its year-end target for the S&P 500 to 6,600, up from previous forecasts, and set a June 2026 goal of 6,800, pointing to robust earnings growth and improving macroeconomic conditions. The index now appears to have considerable room for upside if earnings momentum continues.

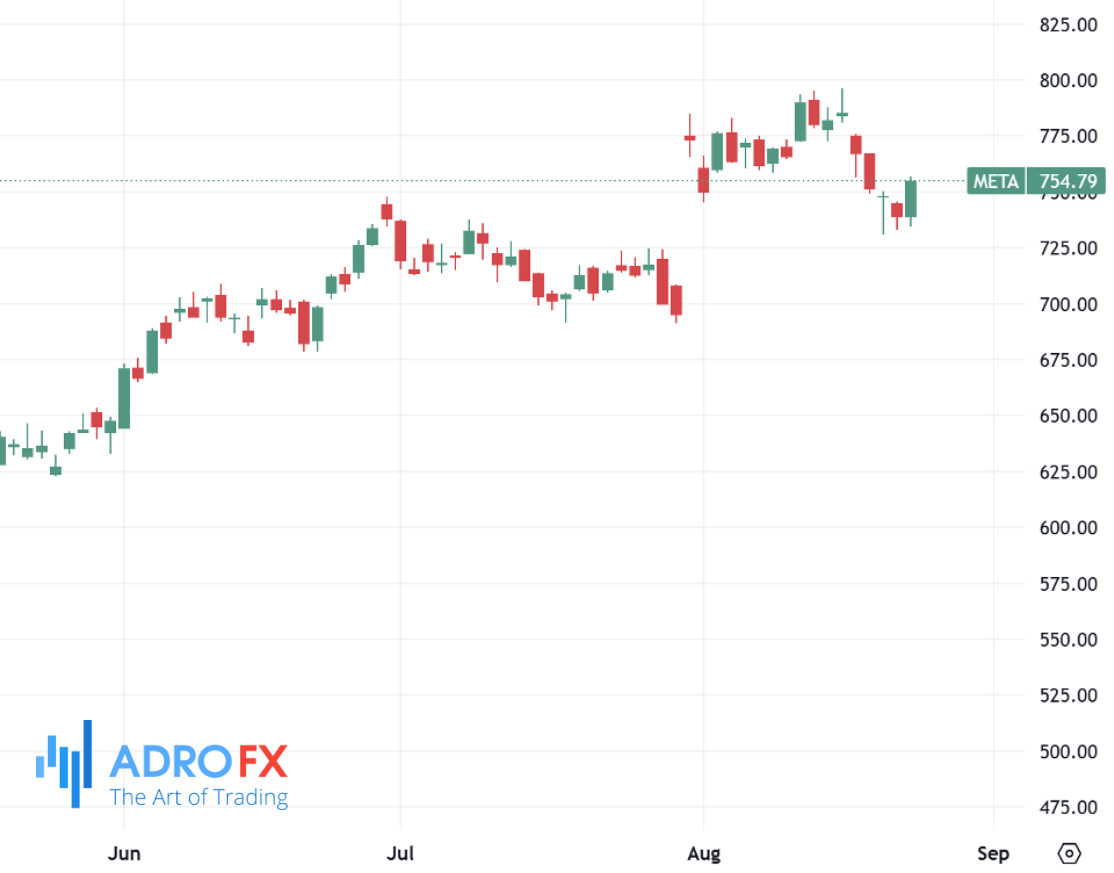

In corporate news, a major development emerged as Meta Platforms finalized a $10 billion agreement with Alphabet’s Google that will see Meta utilize Google Cloud’s infrastructure for servers, storage, and other services over the next six years. This deal underscores the competitive race among large technology firms, often dubbed the “AI Hyperscalers”, to develop advanced artificial intelligence capabilities. With investors demanding tangible returns on the billions invested in AI infrastructure, such partnerships are expected to play a critical role in accelerating innovation while containing costs.

Currency markets began the new week adjusting to the shifting outlook on US rates. The New Zealand dollar weakened against the US dollar, with NZD/USD slipping back to around 0.5860 in Monday’s Asian trading. The move followed a stronger-than-expected retail sales report that showed consumer spending rising 0.5% in the second quarter, easing from the previous quarter’s 0.8% but comfortably ahead of forecasts for 0.2%. Excluding autos, sales rose 0.7%, marking a healthy sign of domestic demand. Even so, last week’s decision by the Reserve Bank of New Zealand to cut its Official Cash Rate by 25 basis points to 3%, a three-year low, continued to weigh on sentiment. Prime Minister Christopher Luxon criticized the central bank’s action, arguing that a deeper reduction was necessary to revive momentum in an economy still struggling with weak growth.

Gold prices retreated slightly in Asian trading, with spot prices near $3,350 per ounce as a firmer dollar offset some of the optimism surrounding an imminent Fed rate cut. Powell’s comments at the Jackson Hole symposium left the door wide open for easing in September, though he cautioned that rising inflationary pressures could complicate the path forward. The Fed chair highlighted a difficult balancing act, noting that risks were now tilted toward higher inflation on one hand and softening employment on the other. For gold, the dovish tone offered some support, as lower interest rates reduce the opportunity cost of holding non-yielding assets. At the same time, geopolitical developments provided another layer of uncertainty: Ukrainian President Volodymyr Zelensky vowed that his nation would continue to defend its sovereignty on Independence Day, a defiant response to Russia’s ongoing military pressure. Reports emerged that drone strikes had targeted Russian energy facilities, including a fire at a nuclear power plant in the Kursk region, raising concerns over potential escalation.

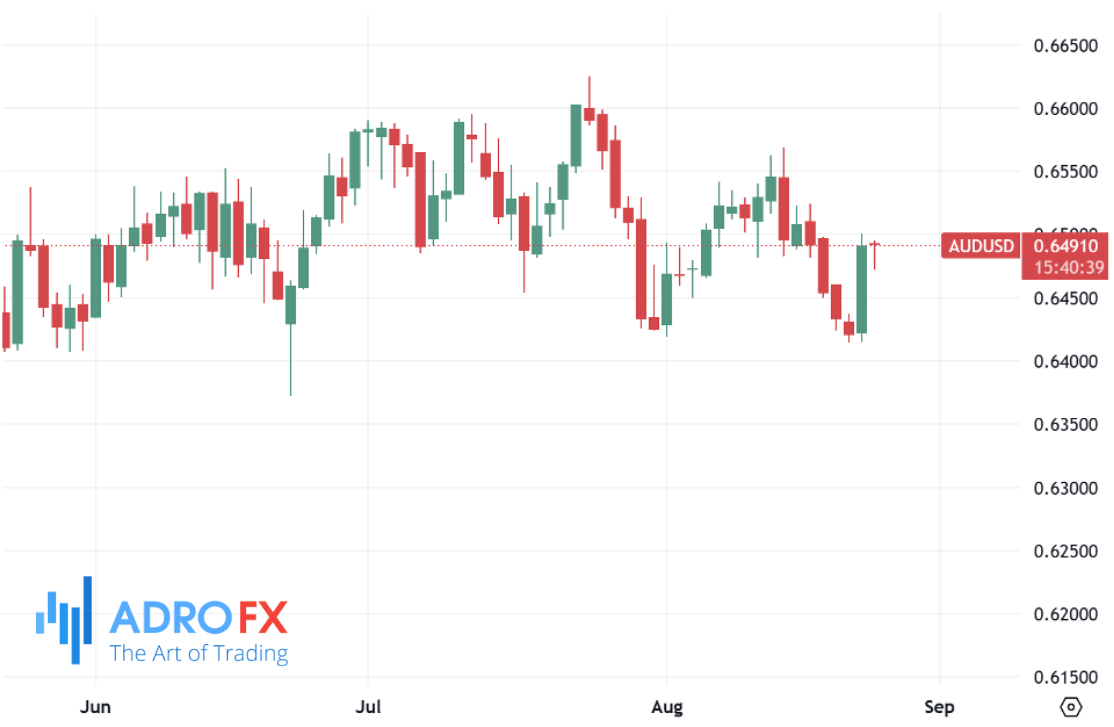

The Australian dollar also lost some ground after its recent rally, slipping against the greenback on Monday. Traders remained cautious about the Reserve Bank of Australia’s next move after its most recent rate cut, with speculation that a larger 50 basis point cut could come as soon as November if economic conditions deteriorate. The cautious tone reflects the central bank’s challenge of balancing inflation risks with a slowing domestic economy, as investors remain highly sensitive to signals about the RBA’s policy trajectory.

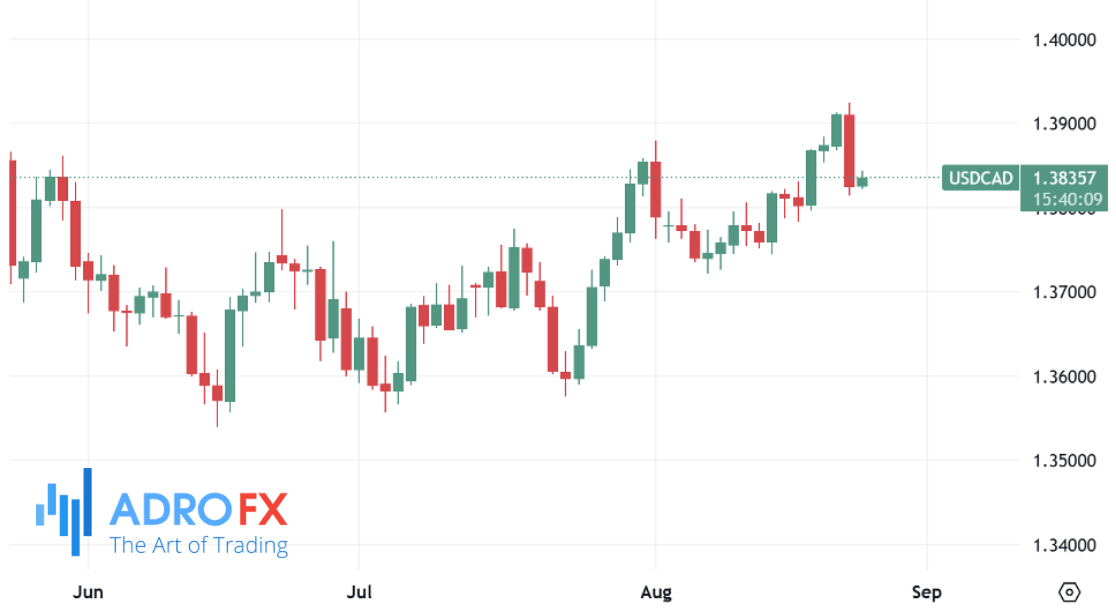

North of the border, the Canadian dollar struggled to regain its footing after USD/CAD slid nearly 0.8% to 1.3820 late last week. The pair stayed subdued in Asian trading as Powell’s dovish tilt reinforced the notion that US policy was likely to loosen in the months ahead, potentially weighing on the dollar.

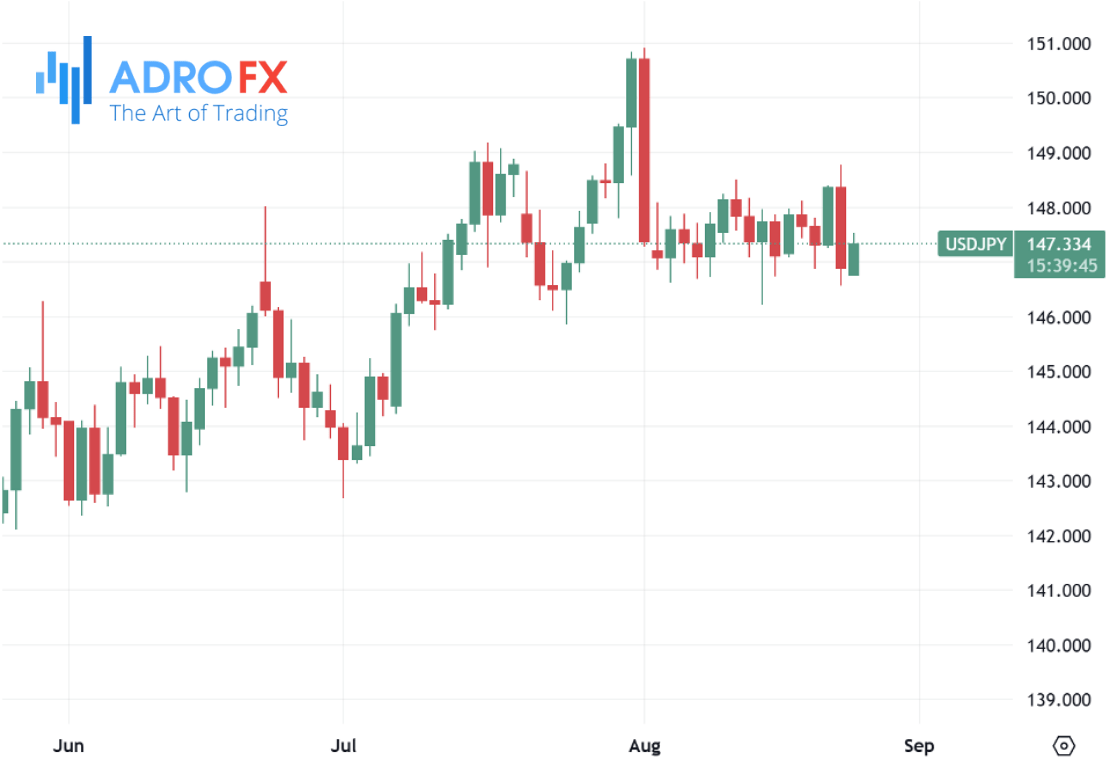

The Japanese yen, meanwhile, faced renewed volatility. USD/JPY rose toward 147.40 after dropping by about 1% in the prior session. Gains for the dollar were capped, however, as remarks from Bank of Japan Governor Kazuo Ueda suggested that another rate hike could be on the horizon. Ueda expressed confidence that wage growth was spreading beyond large corporations to smaller firms, reinforcing the view that Japan’s tightening labor market was creating the conditions necessary for sustainable inflation. Despite July data showing a slowdown in core inflation to 3.1% from earlier peaks, the figure remained above the BoJ’s 2% target, keeping expectations alive that policy normalization could continue.

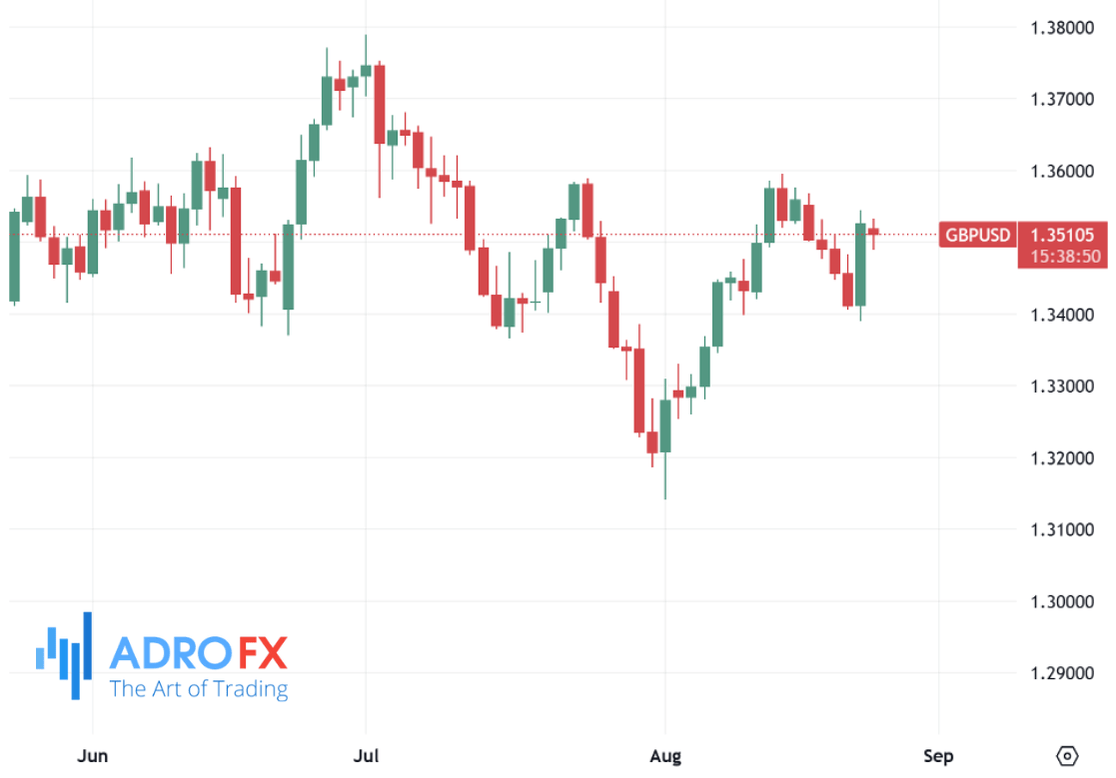

In the United Kingdom, sterling traded lower at around 1.3495 against the dollar during early Monday trading. Renewed dollar strength weighed on the pair, though expectations around future Bank of England policy offered some support. A hotter-than-anticipated July inflation report has led markets to scale back expectations for imminent BoE easing. The central bank recently trimmed its key rate from 4.25% to 4.0% as part of what it described as a gradual and careful approach to policy, but a fresh cut is not fully priced in until March 2026. In the short term, GBP/USD is expected to remain driven by dollar dynamics, with limited UK data scheduled for release this week.

Looking ahead, investors are preparing for a busy economic calendar in the United States. Key releases include July’s durable goods orders and the Personal Consumption Expenditures Price Index, the Fed’s preferred measure of inflation. Both data points will be closely scrutinized as markets attempt to reconcile Powell’s dovish language with the reality of inflation pressures that remain uncomfortably high. Global markets are likely to remain volatile as traders weigh central bank actions, geopolitical tensions, and shifting corporate strategies in the months ahead.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates