Tech Breather Leads S&P 500 Lower While Boeing Announces Management Shake-Up | Daily Market Analysis

Key events:

- USA - Durable Goods Orders (MoM) (Feb)

- USA - CB Consumer Confidence (Mar)

Monday witnessed a decline in the S&P 500 as major tech players took a breather, anticipating pivotal market events later in the week, including an update on inflation and statements from Federal Reserve officials.

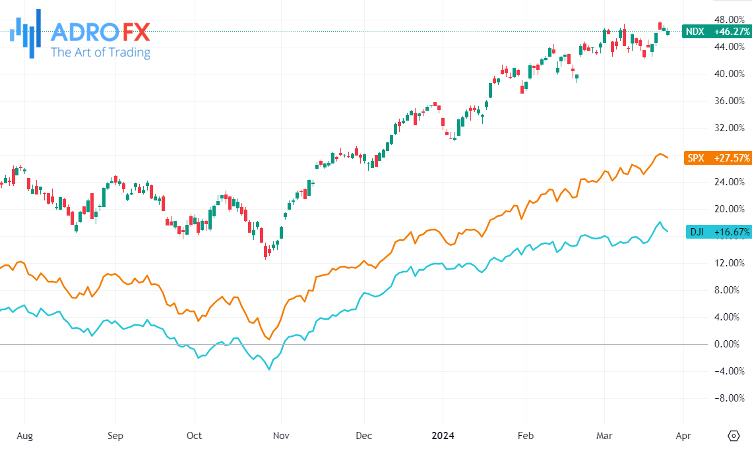

The Dow Jones Industrial Average dipped by 162 points, or 0.4%, while the S&P 500 experienced a 0.3% drop, and the NASDAQ Composite slipped by 0.3%.

In contrast, gold prices ascended on Monday, striving to stabilize following recent fluctuations as the dollar's strength subsided and gold ETFs observed their first inflow ahead of forthcoming remarks from Federal Reserve members and a crucial inflation report later this week.

According to a recent report by RBC, physical gold ETFs welcomed their first weekly inflow of the year, totaling a substantial 483,000 ounces. These signs of investor interest in ETFs emerged shortly after the Federal Reserve maintained its stance on three potential rate cuts this year.

Despite this, the dollar index reversed its gains, falling by 0.3% on Monday, even as certain Fed members expressed uncertainty regarding the necessity of three rate cuts this year.

Atlanta Federal Reserve Bank President Raphael Bostic reiterated on Monday that he sees the need for only one rate cut this week, emphasizing that the robust economy enables the central bank to proceed cautiously.

Similarly, Fed Governor Lisa Cook emphasized the importance of exercising prudence in rate cuts. These less dovish remarks contrast with Fed Chairman Powell's recent speech, following the central bank's indication that three rate cuts are still under consideration for 2024.

Further commentary from the Federal Reserve is anticipated later this week, with remarks from Fed Governor Christopher Waller and Chairman Jerome Powell expected to draw significant investor attention.

In other news, Boeing (NYSE: BA) announced significant management changes on Monday. Dave Calhoun is set to step down as CEO by the end of 2024, while Board Chair Larry Kellner has indicated he will not stand for re-election at the upcoming Boeing annual shareholder meeting. Steve Mollenkopf will succeed Kellner as independent board chair.

Additionally, Stan Deal, Boeing Commercial Airplanes President, and CEO, will retire from the company, with Stephanie Pope appointed to lead the unit effective immediately. These changes come amidst a challenging period for Boeing, marked by incidents and issues that have raised concerns regarding the company's quality control, safety standards, and overall governance.

Boeing shares experienced a 3.8% surge at the market open on Monday, briefly surpassing the $196 per share mark before slightly retracting.

During Tuesday's Asian session, the GBP/USD pair maintains a slight positive bias but struggles to sustain upward momentum, lingering below the mid-1.2600s following an overnight swing high. Despite a recent bounce from the 1.2475 area, or a five-week low hit last Friday, the fundamental landscape favors bearish sentiment, urging caution before anticipating further gains.

Last week, Bank of England Governor Andrew Bailey remarked that expectations of interest rate cuts this year were reasonable, reflecting a shift in sentiment among policymakers who previously advocated for rate hikes. This change, coupled with the US Dollar exhibiting resilience on the back of an optimistic economic outlook, acts as a deterrent for the GBP/USD pair to rally.

In the realm of the Australian Dollar, intraday gains are tempered on Tuesday, albeit receiving support from the weakening US Dollar during early Asian trading hours. However, a decline in Australia's Westpac Consumer Confidence data for March 2024 contributes to slight downward pressure on the AUD/USD pair, offsetting some of the initial gains.

The European Central Bank is also in focus as bets increase for a potential rate cut in June, with Bank of Italy Governor Fabio Panetta emphasizing the possibility due to rapidly falling inflation. Additionally, ECB chief economist Philip Lane hinted at the likelihood of interest rate adjustments once wage growth slows and inflation approaches the 2% target. These factors weigh on the EUR/USD pair's upside potential.

Meanwhile, the Japanese Yen maintains a sideways consolidation during Tuesday's Asian session, remaining close to the year-to-date low against the US Dollar touched last week. The Bank of Japan maintains accommodative financial conditions without providing clear guidance on policy normalization, while speculations of intervention by Japanese authorities to curb further JPY weakness persist.

Looking ahead, market participants await key US economic releases including Durable Goods Orders, the Conference Board's Consumer Confidence Index, and the Richmond Manufacturing Index during the North American session. These data points could provide further direction for currency markets.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates