Market Volatility and Policy Uncertainty Dominate End-of-Quarter Headlines | Daily Market Analysis

Key events:

- USA - ISM Manufacturing PMI (Sep)

- USA - ISM Manufacturing Prices (Sep)

- USA - Fed Chair Powell Speaks

Market performance on Friday concluded with slight losses as investors braced themselves for the possibility of a US government shutdown and adjusted their portfolios for the end of the quarter. In a noteworthy development, hardline Republicans in the US House of Representatives rejected their leader's proposed bill to temporarily fund the government, making it highly likely that federal agencies will face a partial shutdown starting on Sunday.

Traders indicated an 85.8% probability that the Fed would maintain interest rates at their current levels during its upcoming meeting in November, up from 80.7% on Thursday, according to the latest data from CME Group's Fedwatch tool.

The price of gold experienced a substantial decline on Friday, capping off September with a decrease of over 4.5%. This marked the second consecutive quarter of losses for the precious metal. Furthermore, gold registered its most significant weekly drop in over two years, primarily due to the growing consensus that the Federal Reserve (Fed) intends to maintain higher interest rates for an extended period. Indeed, the US central bank opted to leave the benchmark rate unchanged during its September meeting but maintained the projection of one more rate hike by year-end.

On Friday, the gold price did briefly rebound following the release of the United States (US) Personal Consumption Expenditures (PCE) Price Index. However, this upward movement quickly lost momentum. The data failed to alter the perception that the Fed will persist in tightening its monetary policy. Consequently, this outlook prompted another surge in US Treasury bond yields on Monday, extending the XAU/USD's decline for the sixth consecutive day.

In the realm of currencies, the US dollar was on track for its most substantial quarterly gain in a year, continuing its winning streak for the 11th consecutive week. Meanwhile, the Japanese yen remained under close scrutiny for potential government intervention.

The yen exhibited a 0.07% weakening against the greenback, with an exchange rate of 149.43 yen per dollar. The dollar index, measuring the dollar against a basket of major currencies, rose by 0.038%, while the euro posted a 0.09% increase to reach $1.0568.

Sterling was last traded at $1.22, reflecting a marginal 0.02% increase, following data indicating that Britain's economic performance since the onset of the COVID-19 pandemic was stronger than previously estimated.

The initial week of October marks the commencement of the fourth quarter, featuring two significant central bank meetings and numerous noteworthy economic events. It's important to note that mainland China's stock markets will remain closed throughout the week in observance of the National Day holiday, with Hong Kong following suit but only on Monday.

To begin, the United States is set to unveil a highly anticipated employment report for September on Friday. Economists anticipate an addition of 163,000 jobs to the economy last month, which represents a slight deceleration from the 187,000 jobs added in August. A reading that surpasses expectations could reinforce the Federal Reserve's commitment to keeping interest rates higher for a longer duration, potentially exerting downward pressure on the financial markets.

Leading up to Friday's report, we will see the release of the JOLTS jobs report for August on Tuesday. This will be followed by the ADP National Employment report, which provides an update on private sector hiring and is expected to indicate a moderation in job growth.

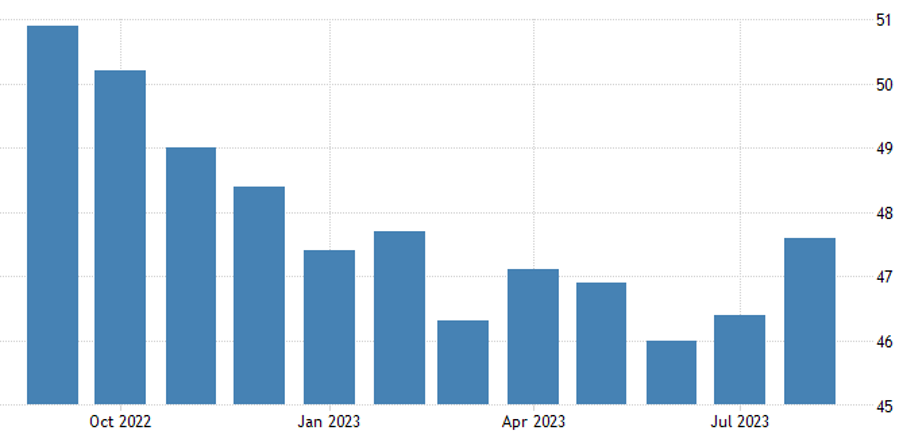

Additionally, on Monday, the Institute for Supply Management will publish its September manufacturing Purchasing Managers' Index (PMI), which is anticipated to remain in contraction territory for the eleventh consecutive month. The ISM services PMI, scheduled for release on Wednesday, is expected to show slightly slower growth.

The fourth quarter is commencing after a lackluster performance in the third quarter for stock markets. During the quarter, the S&P 500 declined by approximately 3.6%, the Dow by 2.6%, and the Nasdaq by 4.1%. In September alone, the S&P 500 dropped by 4.9%, the Dow fell by 3.5%, and the Nasdaq declined by 5.8%.

Heightened bond yields are unsettling stock markets, with concerns arising about the lofty valuations of mega-cap companies such as Apple (NASDAQ: AAPL), Microsoft (NASDAQ: MSFT), Alphabet (NASDAQ: GOOGL), and Amazon (NASDAQ: AMZN) possibly becoming a vulnerability. Stocks of tech and growth-oriented firms, which often rely on robust future profit growth projections, tend to suffer more when bond yields rise, as their expected earnings are discounted more severely.

Nonetheless, the fourth quarter will bring another earnings season. While the AI sector's performance remains crucial, lingering questions persist regarding the extent of its contribution to overall profits.

On Tuesday, the Reserve Bank of Australia will convene its first meeting with new governor Michele Bullock, who is the first woman to lead the bank. Investors will be closely monitoring any hints regarding the RBA's stance on interest rate hikes, especially in light of recent signs of persistent inflationary pressures in the service sector. The consensus, however, leans towards a pause in rate adjustments.

Meanwhile, on Wednesday, the Reserve Bank of New Zealand is scheduled to conduct its latest policy meeting. Despite the RBNZ's hawkish position, market observers do not anticipate a rate hike at this meeting. Instead, the focus will be on any indications from officials about a possible move in November.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates