Global Markets Struggle Amid Weak US Retail Sales, Inflation Concerns, and Geopolitical Uncertainty | Daily Market Analysis

Key events:

- USA - Washington's Birthday

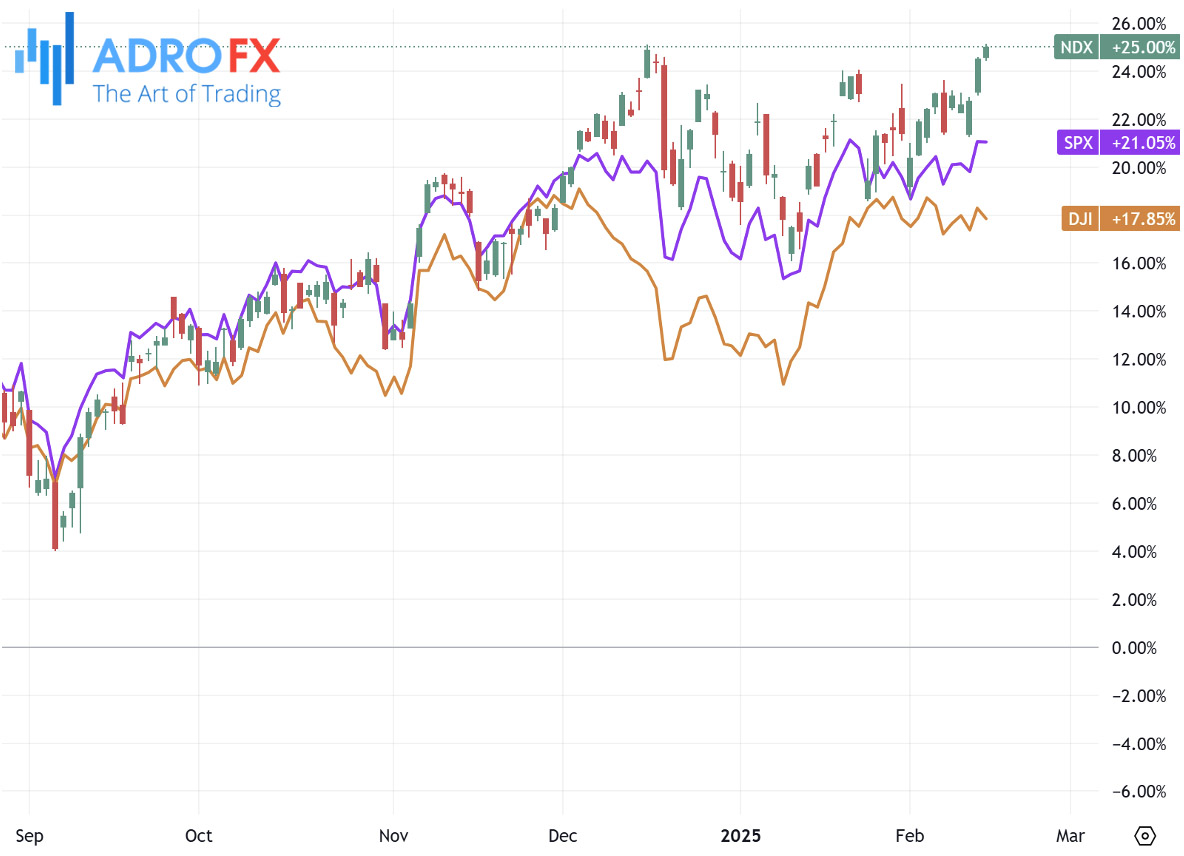

The S&P 500 closed just below its record high on Friday as signs of weakening consumer spending and persistent inflation concerns limited gains.

The Dow Jones Industrial Average declined by 166 points, or 0.4%, while the S&P 500 edged down 0.1% to finish at 6,111.75, just short of its all-time peak of 6,118.71. The NASDAQ Composite remained largely unchanged.

The USD/CHF pair continues its downward trend, slipping toward the 0.8990 level during the early European trading session as the US Dollar faces renewed weakness. Investors are keeping an eye on upcoming speeches from Federal Reserve officials Patrick Harker and Michelle Bowman later today, while Switzerland’s Industrial Production data is set for release on Tuesday.

A steep decline in US retail sales has put additional pressure on the USD. Data from the US Census Bureau revealed that retail sales contracted by 0.9% in January, marking the biggest drop in nearly two years. This was a significant miss compared to market expectations of a 0.1% decline and followed a revised 0.7% increase in December. The weak retail sales report has strengthened market speculation that the Fed could start cutting interest rates as early as June.

Meanwhile, inflation data released this week showed stronger-than-expected consumer and producer price increases. However, certain components of the Producer Price Index (PPI), which influence the Federal Reserve’s preferred inflation measure - the PCE price index - displayed some softness. This could indicate a slightly milder PCE reading for January.

A slowdown in PCE inflation might provide the Fed with more flexibility to lower interest rates, but Fed Chair Jerome Powell cautioned that policymakers would proceed carefully before making further cuts.

On the geopolitical front, officials from the Trump administration are scheduled to meet with their Russian counterparts in Saudi Arabia on Tuesday to discuss potential resolutions to the war in Ukraine. If negotiations lead to progress toward a peace agreement, demand for safe-haven assets such as the Swiss Franc may decrease. However, lingering uncertainties and geopolitical risks could continue to support CHF strength in the near term.

The Australian Dollar extends its winning streak against the USD for the third consecutive day, benefiting from US President Donald Trump’s decision to postpone the implementation of reciprocal tariffs. However, the currency’s upside could be capped as traders brace for the Reserve Bank of Australia meeting on Tuesday. The RBA is widely expected to cut its Official Cash Rate (OCR) by 25 basis points to 4.10%, marking its first rate reduction in four years. If the central bank adopts a more dovish tone, it could limit further gains for the AUD/USD pair.

The Japanese Yen maintains its bullish momentum for the third straight session, supported by expectations that the Bank of Japan will continue raising interest rates. Fresh data showed Japan’s annual GDP growth accelerated to 2.8% in the fourth quarter, up from a revised 1.7% in the previous quarter. This strong performance bolsters the BoJ’s case for further policy tightening amid persistent inflation.

Japan’s Economy Minister Ryosei Akazawa remains optimistic about moderate economic recovery but cautions that downside risks from the global economy should not be ignored. Meanwhile, reports suggest that Japan has requested an exemption from the 25% tariffs on steel and aluminum imposed by the Trump administration.

The New Zealand Dollar attracts buying interest for the third consecutive day, pushing NZD/USD to a two-month peak near 0.5750 during the Asian session. The US Dollar’s continued weakness has supported the pair’s bullish momentum.

However, the possibility of further rate cuts by the Reserve Bank of New Zealand could limit NZD’s upside. The RBNZ is expected to consider another supersized rate cut later this month, which could temper the recent rally in NZD/USD.

From a technical standpoint, last week’s breakout above the key 0.5700 level suggests that bullish momentum remains intact. Any pullbacks may present buying opportunities ahead of the crucial RBNZ policy announcement on Wednesday.

Related Articles

Latest updates

Latest updates

Technical Analysis

Latest updates